Country

Companies10 of 16

revolut.com

Revolut

revolut.com🇱🇹 Lithuania

Revolut is a London-born mobile banking platform that turned the idea of a bank in your pocket into reality. It started as a borderless payments app and has evolved into something far more ambitious: a full-stack financial operating system for the smartphone generation. Most traditional banks still treat international transfers as a painful, expensive legacy process. Revolut made them free and instant.

The app combines a debit card, multi-currency accounts, cryptocurrency trading, insurance, and investment tools into a single interface. It's designed for people who spend time across borders, who think in multiple currencies, and who want their financial life streamlined into one place rather than scattered across apps. Founded in 2015, Revolut has grown into one of Europe's most recognizable fintech brands, with millions of active users across the continent. The company operates its own banking licenses in multiple jurisdictions, giving it the regulatory foundation to move fast where traditional banks move cautiously.

What sets Revolut apart is its refusal to accept friction as inevitable. Travel shouldn't require currency conversion fees. Payments shouldn't require knowing IBAN codes. Investing shouldn't require a separate broker account. In the broader fintech landscape, Revolut represents the shift toward unbundled, mobile-first financial services that challenge the notion that banking needs to be complicated.

Categories

Digital BankingPaymentsWealthCrypto & BlockchainPersonal Finance

neofinance.com

NeoFinance

neofinance.com🇱🇹 Lithuania

Lithuanian peer-to-peer lending built one of the more substantial European markets for marketplace consumer credit, with multiple platforms competing for both borrowers and investors in a country that has cultivated a regulatory environment supportive of fintech experimentation. NeoFinance was founded in Vilnius in 2014 as one of those Lithuanian P2P pioneers, connecting Lithuanian and international investors with creditworthy local borrowers seeking personal loans. The platform's domestic focus gave it credit data depth in the Lithuanian market that pan-European platforms didn't match, while its EU passport allowed it to attract investor capital from across Europe. NeoFinance has expanded its operations and product range while navigating the maturation of European P2P lending — including the regulatory tightening that brought retail crowdfunding under the European Crowdfunding Service Provider Regulation framework. In the Lithuanian P2P landscape, NeoFinance represents one of the longer-running platforms operating with a domestic borrower focus and a Pan-European investor base — a combination that has proven more sustainable than purely cross-border models that lacked deep credit knowledge of any single market.

Categories

Lending

paysera.com

Paysera

paysera.com🇱🇹 Lithuania

Paysera is a Lithuanian fintech company that has quietly built one of Europe's most comprehensive payment and banking platforms, serving millions of users across the continent. Rather than chasing hype, Paysera focuses on practical utility—combining payment processing, digital accounts, currency exchange, and invoicing tools into a single interface that works across borders and languages. The platform powers everything from freelancers managing invoices to SMEs handling payroll, while also offering consumer-facing services like multi-currency wallets and competitive exchange rates. What sets Paysera apart is its unglamorous pragmatism: it solves real friction in how Europeans move, spend, and manage money across different countries, without the startup theatrics. It's the kind of company that doesn't dominate headlines but has become indispensable infrastructure for a significant portion of the continent's digital economy. In the crowded European fintech landscape, where newer players chase consumer attention and legacy banks chase compliance, Paysera operates in the profitable middle—trusted by businesses and individuals who value reliability and cross-border simplicity over brand prestige.

Categories

Financial InfrastructurePaymentsDigital BankingSME Finance

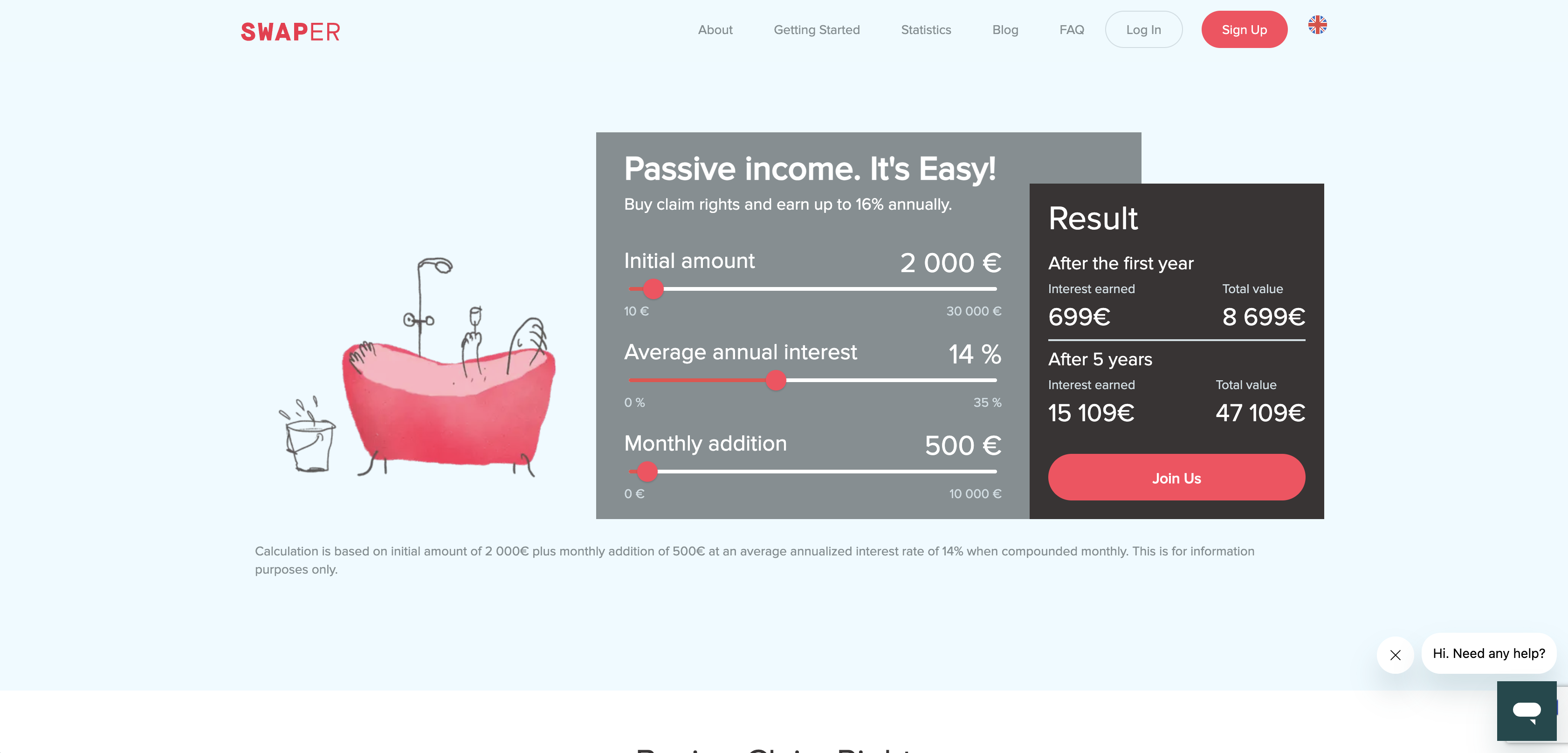

swaper.com

Swaper

swaper.com🇱🇹 Lithuania

Swaper is a peer-to-peer lending platform that connects individual borrowers with investors across Europe, operating since 2014. The platform cuts out traditional banks from the equation, letting regular people lend to and borrow from each other directly—think of it as crowdsourcing credit. It's a refreshingly transparent approach to lending where returns aren't hidden behind opaque fee structures, and borrowers get access to capital without the gatekeeping that conventional banks impose.

The platform operates across multiple European markets, offering investors the chance to diversify their portfolios by backing loans at varying risk levels, while borrowers get competitive rates without the bureaucratic friction. Swaper essentially democratizes what was once a monopoly: the decision about who deserves credit and at what price. For investors looking beyond traditional savings accounts, it's a way to put capital to work. For borrowers, it's an alternative when bank doors close.

In a market still dominated by legacy banking, Swaper represents a more distributed model of credit allocation. It hasn't disrupted traditional lending in the way some fintechs have, but it's quietly built a genuine two-sided marketplace where humans fund humans—no algorithms pretending to be wisdom, just real supply meeting real demand. It's the kind of service that feels more honest than what you'll find at your local bank branch.

Categories

Lending

whitebit.com

WhiteBIT

whitebit.com🇱🇹 Lithuania

WhiteBIT operates as one of the larger cryptocurrency exchanges with European operational presence, offering spot trading, margin trading, and a range of other crypto financial products to a substantial international user base. The exchange has built its position through the combination of competitive trading fees, broad asset coverage, and operational scale that allows it to compete in the same segment as larger international platforms. The European operational base reflects the broader pattern of crypto exchanges seeking jurisdictions with clearer regulatory frameworks and operational viability. WhiteBIT has navigated the evolving European regulatory environment for crypto asset service providers, including the MiCA framework that has reshaped expectations for crypto exchanges operating in or serving European users. The platform's product range covers spot trading, derivatives, staking, and other yield-bearing crypto products that constitute the core of contemporary crypto exchange offerings. In the European crypto exchange landscape, where the regulatory implementation under MiCA is creating new operational requirements and clearer competitive boundaries, exchanges with established operational scale have advantages relative to newer entrants but face the same compliance investment requirements as everyone else. The exchange category continues to consolidate around a smaller number of larger operators with the regulatory standing and operational scale to compete effectively under the formalising European framework.

Categories

Crypto & Blockchain

coingate.com

CoinGate

coingate.com🇱🇹 Lithuania

Accepting cryptocurrency payments as a merchant has always been technically possible and operationally difficult. The volatility of crypto assets, the complexity of wallets, and the absence of chargebacks — seen as a feature by some, a problem by merchants — made crypto payment acceptance a niche choice for most businesses. CoinGate was founded in Vilnius in 2014 to make crypto payment acceptance as straightforward as card payment acceptance, offering a payment gateway that handles the technical and commercial complexity of crypto transactions and settles merchants in euros. Its platform supports over 70 cryptocurrencies, integrates with major e-commerce platforms, and provides the invoicing, reporting, and settlement infrastructure that businesses need to treat crypto payments as a normal part of their payment stack. CoinGate has processed hundreds of millions in transactions and built a merchant network across Europe and beyond. In the Lithuanian fintech ecosystem — which has become disproportionately important in European crypto regulation thanks to the Bank of Lithuania's pragmatic licensing approach — CoinGate represents the merchant-facing end of the crypto payment stack, building the commercial infrastructure that turns cryptocurrency from a speculative asset into a practical payment method.

Categories

Crypto & BlockchainPayments

spectrocoin.com

SpectroCoin

spectrocoin.com🇱🇹 Lithuania

The early years of European crypto were defined by a small number of platforms trying to build the full stack — exchange, wallet, card, and payment gateway — without the regulatory clarity or capital to do it properly. SpectroCoin was founded in Vilnius in 2013 as one of the more ambitious of those early attempts, offering a crypto exchange, a Bitcoin debit card, a payment gateway for merchants, and multi-currency wallet functionality under a single platform. Its early Visa and Mastercard Bitcoin debit card — one of the first in Europe — was a genuine innovation that let crypto holders spend their holdings at any card-accepting merchant without converting in advance. The company received an Electronic Money Institution licence from the Bank of Lithuania, giving it the regulatory standing to issue payment cards and hold electronic money — a licence that the Bank of Lithuania was granting to crypto-adjacent businesses at a time when most European regulators were more cautious. SpectroCoin operates as part of the Bankera ecosystem, which has expanded into banking and lending products. In the Baltic crypto infrastructure landscape, SpectroCoin represents the early-mover generation — platforms that built the first European crypto financial products before the regulatory frameworks existed and that have survived the subsequent decade of market cycles and regulatory evolution.

Categories

Crypto & BlockchainPayments

mistertango.com

Mistertango

mistertango.com🇱🇹 Lithuania

Multi-currency accounts for European businesses and individuals who operate across borders have moved from a specialist need to a mainstream expectation over the past decade. Mistertango was founded in Vilnius in 2016 to serve that market with a Lithuanian electronic money institution offering multi-currency IBAN accounts, payment cards, and digital banking services to retail and business customers across Europe. The Lithuanian regulatory base is significant — the Bank of Lithuania has built one of Europe's most accessible licensing regimes for fintechs, and Vilnius has emerged as a Pan-European fintech hub with disproportionate concentration of EMI licences relative to the country's size. Mistertango has built a customer base of consumers and small businesses needing multi-currency banking capability without the friction of opening accounts with multiple national banks. Its product range includes virtual cards, business accounts, and payment processing, with a particular focus on customers who would otherwise struggle to access banking services from incumbent institutions. In the Lithuanian fintech landscape, Mistertango represents the mid-tier of EMI-licensed operators — not the largest but with sufficient scale and product depth to maintain a sustainable position serving customer segments that fall between the venture-backed neobanks and the traditional banks.

Categories

Digital BankingPayments

neopay.online

Neopay

neopay.online🇱🇹 Lithuania

The Lithuanian Bank's pragmatic approach to fintech licensing has produced a concentration of electronic money institutions and payment service providers that is disproportionate to the country's economy. Neopay was founded in Vilnius in 2015 as one of the EMI-licensed operators serving the European fintech market, providing payment processing, IBAN account services, and card programme infrastructure to businesses and platforms across the EEA. The Lithuanian EMI passport gives Neopay the regulatory standing to offer payment services across all 30 EEA member states without needing additional national licences — the kind of cross-border efficiency that European regulators designed the EMI framework to enable. Neopay's product range serves merchants needing payment acceptance and platforms needing white-label financial infrastructure, operating in the layer of European fintech that exists primarily as B2B infrastructure rather than consumer-facing products. In the broader Lithuanian fintech ecosystem, where dozens of EMI operators compete for similar market segments, Neopay's positioning emphasises the operational reliability and regulatory standing that institutional clients require — a different competitive axis from the consumer-facing fintechs that dominate Lithuanian fintech press coverage but a meaningful one in the wholesale infrastructure layer.

Categories

PaymentsFinancial Infrastructure

connectpay.com

ConnectPay

connectpay.com🇱🇹 Lithuania

Banking-as-a-Service through Lithuanian EMI infrastructure has become a Pan-European pattern — fintech and platform companies needing payment accounts, IBANs, and card programmes increasingly partner with Lithuanian-licensed providers to offer those capabilities under their own brands. ConnectPay was founded in Vilnius in 2018 to provide that BaaS infrastructure to fintechs, payment platforms, and digital businesses across the EEA. Its platform offers IBAN accounts, payment processing, payment cards, and the regulatory infrastructure needed to operate financial products compliantly under partnership arrangements. The company received a full EMI licence from the Bank of Lithuania, giving it Pan-European passporting rights and the regulatory standing to support clients building consumer and business financial products across European markets. ConnectPay's position is in the wholesale layer of European fintech — invisible to consumers but essential to the products they use, with operational scale built on serving multiple platform clients rather than building a direct consumer brand. In the competitive Lithuanian EMI landscape, where dozens of operators target similar B2B clients, ConnectPay's growth reflects the underlying expansion of European embedded finance — every additional non-financial company adding payment or account capabilities to its product creates demand for the kind of infrastructure that ConnectPay provides.

Categories

Financial InfrastructurePaymentsEmbedded Finance