Country

Companies10 of 47

orangebank.fr

Orange Bank

orangebank.fr🇫🇷 France

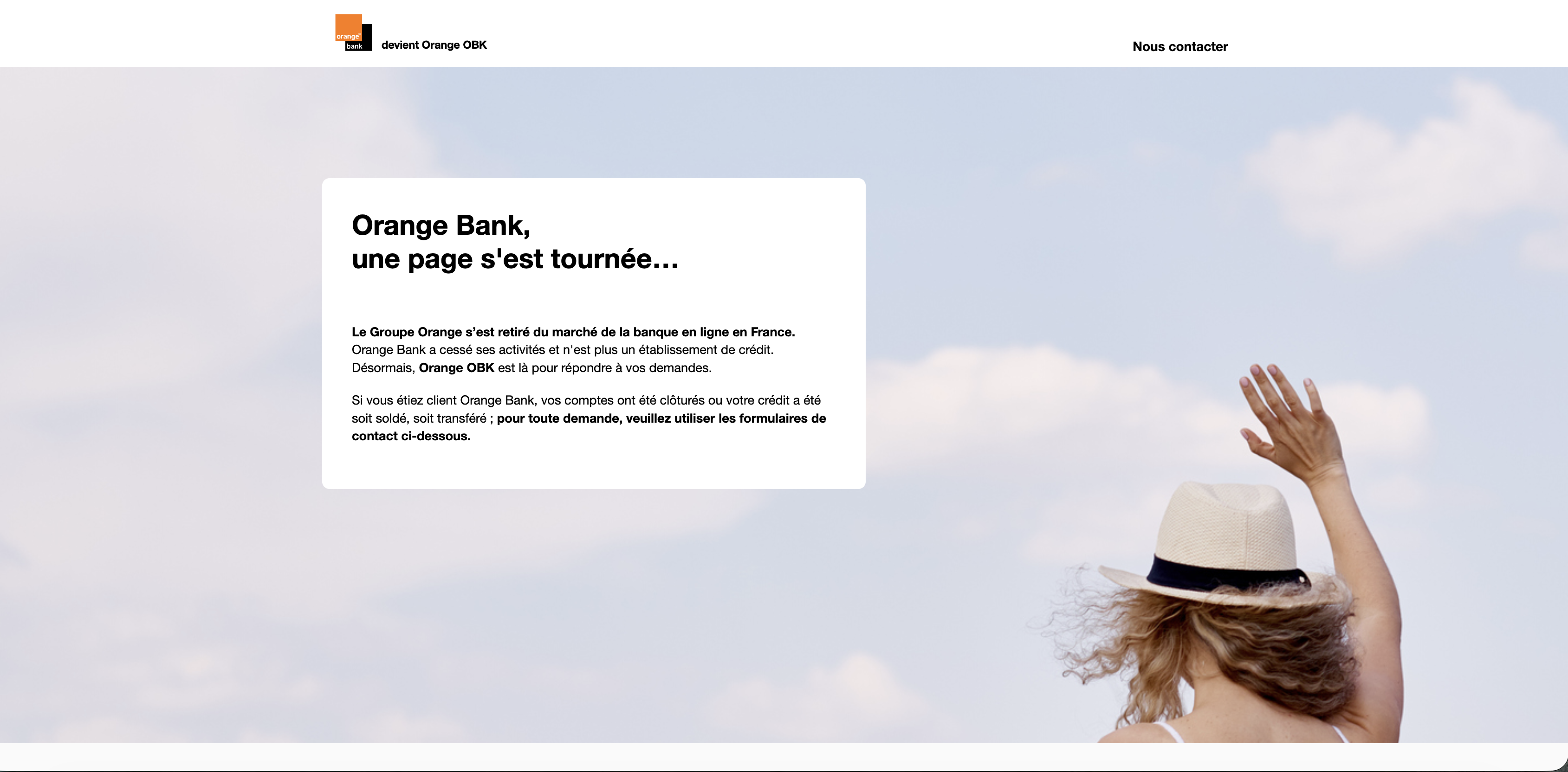

Orange Bank is France's straightforward answer to digital banking, born from the telecom giant Orange's pivot into retail finance. Rather than reinventing the wheel with flashy features, it focuses on delivering genuine utility: competitive savings rates, no-fee accounts, and a mobile experience that feels native to French users who already trust Orange's infrastructure. The brand trades on Orange's massive distribution reach and existing customer relationships, offering a credible alternative to both traditional banks and the newer neobank crowd. Where many challenger banks chase viral growth, Orange Bank plays the long game—leveraging a parent company with real retail presence across France. It's banking designed for people who want simplicity without sacrificing control: straightforward pricing, transparent terms, and the backing of one of Europe's largest telecoms. In the European digital banking landscape, Orange Bank represents a hybrid model: the scale and trust of an incumbent, the agility and user focus of a challenger. It proves you don't need to be born digital to compete in digital—you just need to execute without the legacy baggage.

But execution, as it turned out, was precisely where the story became more complicated. Despite its strong foundations, Orange Bank struggled to achieve the scale and profitability needed to justify its ambitions. Customer acquisition proved slower and more expensive than expected, and the competitive pressure from nimble fintech players—and increasingly digitized traditional banks—tightened margins. What was meant to be a steady, long-term play began to look like a costly experiment.

Eventually, Orange made the pragmatic decision to step back. The bank began winding down its retail operations, marking a quiet end to a bold attempt at convergence between telecom and finance. For customers, the impact was managed and orderly. For the industry, however, it served as a clear signal: brand trust and distribution alone are not enough to win in digital banking.

The lesson from Orange Bank isn’t that incumbents can’t innovate—it’s that entering financial services requires more than adjacency and scale. It demands relentless focus, deep specialization, and a willingness to compete in a space where margins are thin and expectations are high. Orange Bank showed what’s possible when a non-bank enters finance—but also highlighted just how hard it is to stay there.

Categories

Digital Banking

qonto.com

Qonto

qonto.com🇫🇷 France

Qonto is a European business banking platform that treats SMEs and freelancers the way tech-forward founders wish their banks would: fast, transparent, and built for how modern companies actually operate. Instead of waiting days for payments to clear or wrestling with legacy banking interfaces, Qonto users get instant payments, real-time visibility across their accounts, and integrations that sync seamlessly with their existing tools.

The platform lives at the intersection of traditional banking and fintech simplicity. Qonto handles everything from multi-currency accounts and payment processing to expense management and financial reporting, all from a mobile-first interface that feels like an app, not a bank. The company has quietly become the go-to choice for growing SMEs across Europe who want banking that doesn't slow them down.

What sets Qonto apart in a crowded B2B banking space is its obsessive focus on the user experience and its commitment to European expansion. While many neobanks either chase mass-market consumers or hide behind enterprise complexity, Qonto sits in a sweet spot: accessible enough for a solo founder, powerful enough for teams managing millions in annual revenue. The company's growth across France, Germany, Spain, Italy, and beyond reflects a simple truth: European businesses have been waiting for a bank that understands their needs.

As European business banking undergoes its biggest transformation in decades, Qonto stands as proof that the future of SME finance isn't about moving fast and breaking things—it's about moving fast and building things that actually work.

Categories

PaymentsDigital BankingSME Finance

payfit.com

PayFit

payfit.com🇫🇷 France

PayFit is a French payroll and HR software platform that automates the tedious work of managing employee compensation, benefits, and compliance across Europe. Founded in 2015, the company has built something genuinely useful: a system that lets mid-market companies and SMEs stop wrestling with spreadsheets and outdated payroll systems, and instead manage their entire workforce in one place.

The platform handles everything from salary calculations and tax filings to expense reports and leave management—work that traditionally demanded a dedicated HR department or expensive outsourcing. What sets PayFit apart is its focus on reducing administrative friction rather than just digitizing existing processes. The interface feels designed for actual users, not consultants. It integrates with accounting software and handles the increasingly complex regulatory landscape across France, Germany, Spain, and the UK, where employment law differs wildly but payroll headaches remain universal.

In Europe's fragmented payroll software market, where legacy providers still dominate through inertia, PayFit represents a generational shift toward cloud-first, mobile-friendly HR operations. The company competes less on features (though it has plenty) and more on making payroll feel like a solved problem rather than an annual migraine. It's the kind of infrastructure play that startups and growth companies build themselves around once they've used it—not flashy, but fundamentally necessary.

Categories

SME Finance

kyriba.com

Kyriba

kyriba.com🇫🇷 France

Kyriba is a cloud-native treasury and finance platform that sits at the intersection of corporate finance operations and intelligent automation. Rather than patching together spreadsheets and legacy systems, Kyriba consolidates cash management, liquidity forecasting, and working capital visibility into a single operating system for finance teams. Think of it as the command center for CFOs who are tired of fragmented data and manual workflows.

The platform handles everything from multi-currency cash positioning to FX hedging and supply chain financing, all orchestrated through APIs that plug into banks and accounting systems. It's built for mid-market to enterprise companies that move serious money across borders and need to know exactly where every dollar sits at any given moment. Kyriba doesn't try to be a banker or a startup darling—it's an industrial-grade tool that speaks the language of corporate treasurers.

In the European treasury space, Kyriba competes with legacy software vendors but with a modern cloud architecture that actually scales. It's the kind of platform that gets adopted quietly but becomes mission-critical once companies realize how much time their finance teams get back. The market for treasury automation remains sticky and consolidating, but Kyriba has built a defensible position by solving the unglamorous but essential work of helping large corporations optimize their balance sheets and reduce financial risk.

Categories

Treasury

younited-credit.com

Younited Credit

younited-credit.com🇫🇷 France

Younited Credit sits at the intersection of consumer lending and fintech, offering personal loans to borrowers across Europe who want speed and transparency instead of the bureaucratic friction of traditional banks. Founded in 2011, the company has evolved from a peer-to-peer lending marketplace into a full-stack credit platform that sources, prices, and services loans for both retail customers and institutional partners.

The core product is straightforward: quick online approval (often minutes), competitive rates based on real underwriting, and a streamlined digital experience that feels more like ordering something on your phone than sitting in a bank branch. What distinguishes Younited from the crowded European consumer lending space is its scale and sophistication. Rather than just operating a marketplace, the company has built proprietary credit scoring models, automated servicing infrastructure, and a diversified funding model that includes institutional investors, warehouse financing, and securitization. This means Younited isn't dependent on peer-to-peer investors or a single funding source—it can grow independently. The platform operates across multiple European markets and has become a quiet infrastructure player for consumer credit, processing loans for direct borrowers while also powering lending for third parties through white-label partnerships. In an era when legacy banks still treat personal lending like a commodity and fintechs are scrambling to prove unit economics, Younited represents the pragmatic middle ground: technology-first underwriting and customer experience wrapped around a business model that actually scales profitably.

Categories

LendingPersonal Finance

ledger.com

Ledger

ledger.com🇫🇷 France

Ledger is the world's most recognizable cryptocurrency hardware wallet manufacturer, though the company has evolved well beyond that single product. Founded in 2014, it pioneered the idea that self-custody of digital assets could be both secure and user-friendly, making crypto accessible to millions who otherwise would have left their holdings on exchanges. The company operates as a full-stack crypto infrastructure provider, offering hardware wallets (Ledger Nano S and X), a software wallet platform, and developer APIs that let third-party services integrate Ledger's security model into their own products.

What sets Ledger apart in the crypto space is its obsessive focus on security through isolation. While competitors often offer software wallets or custodial solutions, Ledger's approach keeps private keys permanently offline, eliminating the attack surface that plagues hot wallets. The company has successfully maintained that zero-breach record for a decade, which matters enormously in an industry built on trust and skepticism. Beyond hardware, Ledger has quietly built a platform ecosystem—Ledger Live (the official app) aggregates portfolio tracking, staking, swaps, and third-party integrations, turning the wallet into something closer to a financial operating system for crypto natives.

Ledger operates at a fascinating intersection of consumer hardware business and B2B infrastructure play. Millions of individual users buy Ledger devices directly, but the company also licenses its technology to banks, exchanges, and other financial institutions looking to offer institutional-grade custody. It's a rare position in fintech: simultaneously a consumer brand (few non-crypto companies sell physical products as recognizable as a Ledger Nano) and an enterprise security provider. That duality has made Ledger one of Europe's most valuable fintech unicorns, though it remains private. In the broader fintech ecosystem, Ledger represents the backbone layer—the infrastructure that makes decentralized finance possible without requiring users to become security experts themselves.

Categories

Crypto & Blockchain

anaxago.com

Anaxago

anaxago.com🇫🇷 France

Anaxago is a European investment platform that democratizes access to private market deals, letting retail investors back startups and SMEs that would normally require deep pockets and insider connections. The platform sidesteps the gatekeeping that has long defined venture capital, offering curated equity stakes in growth-stage companies across tech, real estate, and other sectors. Founded in 2014, it operates across multiple European markets and has processed hundreds of millions in investments, positioning itself as a bridge between ambitious entrepreneurs and everyday investors seeking portfolio diversification beyond public markets. What sets Anaxago apart is its focus on transparency and accessibility. Rather than opaque fund structures or minimum investment requirements that exclude ordinary savers, it lets users invest from relatively modest amounts while maintaining rigorous due diligence on every deal. The platform handles the mechanics of investment management, shareholder rights, and secondary market liquidity—functions that typically require armies of lawyers and compliance teams. It's part of a broader shift toward democratized finance, where technology makes previously exclusive opportunities available to anyone with capital and appetite for risk. In the European fintech landscape, where crowdfunding and alternative investment platforms have proliferated, Anaxago has carved out credibility through regulatory compliance, deal flow quality, and a genuine commitment to investor protection. It represents how fintech can unbundle traditional wealth management, making private market exposure a normal part of retail investing rather than a privilege reserved for the wealthy.

Categories

Embedded FinanceWealth

swan.io

Swan

swan.io🇫🇷 France

Swan is reshaping how European businesses handle payments by offering a modern, developer-friendly infrastructure layer that sits between companies and the complexity of traditional banking rails. Rather than forcing startups and established firms to navigate fragmented payment ecosystems, Swan bundles together payment processing, banking APIs, and compliance tooling into a single, coherent platform.

The company targets mid-market and enterprise customers—think e-commerce platforms, SaaS businesses, and financial services—who need to embed payments into their core operations without hiring a dedicated payments team. Swan's core strength lies in its ability to strip away legacy banking friction: it handles card processing, instant payments, payouts, and cross-border transfers through a unified API, while managing the regulatory headaches that usually consume engineering bandwidth.

In a European landscape crowded with payment gateways and banking APIs, Swan distinguishes itself through developer experience and architectural clarity. Where competitors often bolt together disparate services, Swan presents a genuinely integrated stack—one codebase, one dashboard, one billing model. The company serves as both a payments operator and a bridge to traditional banking, making it particularly valuable for businesses scaling beyond their first million transactions.

Swan represents a broader maturation in European fintech infrastructure: the shift from "we'll process your payments" to "we'll become your payments backbone," enabling a generation of companies to focus on their core product rather than payment plumbing.

Categories

Financial InfrastructurePaymentsOpen Banking

alan.com

Alan

alan.com🇫🇷 France

Alan is rewriting health insurance for the digital age, stripping away the bureaucratic drag that makes traditional coverage feel like a relic.

The Paris-based insurtech startup treats health protection as something that should integrate seamlessly into daily life rather than a quarterly bill you dread opening. Using AI and real-time data, Alan automates claims processing, cuts administrative friction, and lets users manage their coverage through a clean mobile app. What sets Alan apart is its focus on speed and transparency. Most European health insurers still operate like they're managing paper files; Alan processes claims in days, not months, and explains costs upfront instead of hiding them in fine print.

The company serves both individuals and SMEs across France, Belgium, Spain, and beyond, positioning itself as the insurance provider for people who actually understand technology. In a market where health insurance feels synonymous with frustration, Alan's role is to prove that coverage can be simple, fast, and genuinely customer-centric.

Categories

InsurTech

swile.co

Swile

swile.co🇫🇷 France

Swile tackles the unglamorous but essential problem of employee benefits administration—turning what's typically a bureaucratic nightmare into something that actually works for modern companies. The Paris-based platform bundles meal vouchers, transportation allowances, childcare support, and wellness benefits into a single card and app that employees actually want to use.

Instead of juggling multiple vendor relationships and paper trails, HR teams get one interface to manage everything. Employees scan a card or phone at participating restaurants, shops, and gyms, earning tax-advantaged benefits while employers simplify their compliance burden. It's the kind of boring-but-essential infrastructure that scales across Europe—Swile operates in France, Spain, Italy, and beyond.

What sets Swile apart in the crowded benefits space is its focus on the entire employee lifecycle rather than just one vertical. While competitors obsess over meal vouchers or mobility, Swile positions itself as a comprehensive benefits platform. The company raised significant Series B funding and expanded aggressively across continental Europe, proving that there's real appetite for consolidation here.

Swile represents a broader shift in how European companies think about compensation: less about salary alone, more about total employee experience. By digitizing what was once entirely analog, Swile has become an essential piece of HR infrastructure for mid-market and enterprise employers across the region.

Categories

Embedded FinanceSME Finance