Country

Companies10 of 24

tink.com

Tink

tink.com🇸🇪 Sweden

Tink is a Swedish open banking platform that connects to over 3,000 financial institutions across Europe, solving the friction between fintech ambition and banking reality. Rather than building their own infrastructure from scratch, startups and established financial companies plug into Tink's APIs to instantly access account data, initiate payments, and orchestrate complex financial workflows without dealing with legacy banking plumbing.

The company sits at the intersection of three powerful trends: the shift toward embedded finance, the regulatory tailwinds of PSD2 and Open Banking, and the growing irrelevance of traditional bank APIs. While competitors chase headlines with consumer-facing apps, Tink operates in the less glamorous but infinitely more valuable B2B2C layer—the infrastructure that quietly powers dozens of European fintech winners.

What sets Tink apart is execution at scale. Their data aggregation and payment initiation services work reliably across fragmented European banking systems, which is harder than it sounds. Most fintechs eventually realize they need a Tink-like layer to escape the nightmare of maintaining connections to hundreds of banks with different technical standards and frequent updates.

That importance hasn’t gone unnoticed. In 2022, Tink was acquired by Visa, a move that underscored just how critical open banking infrastructure has become. The acquisition gave Tink both validation and reach, positioning it even closer to the core of the global payments ecosystem.

Tink represents the unglamorous backbone of modern European fintech—the kind of company that doesn't dominate headlines but becomes quietly indispensable to everyone building financial products.

Categories

Embedded FinanceFinancial InfrastructureOpen Banking

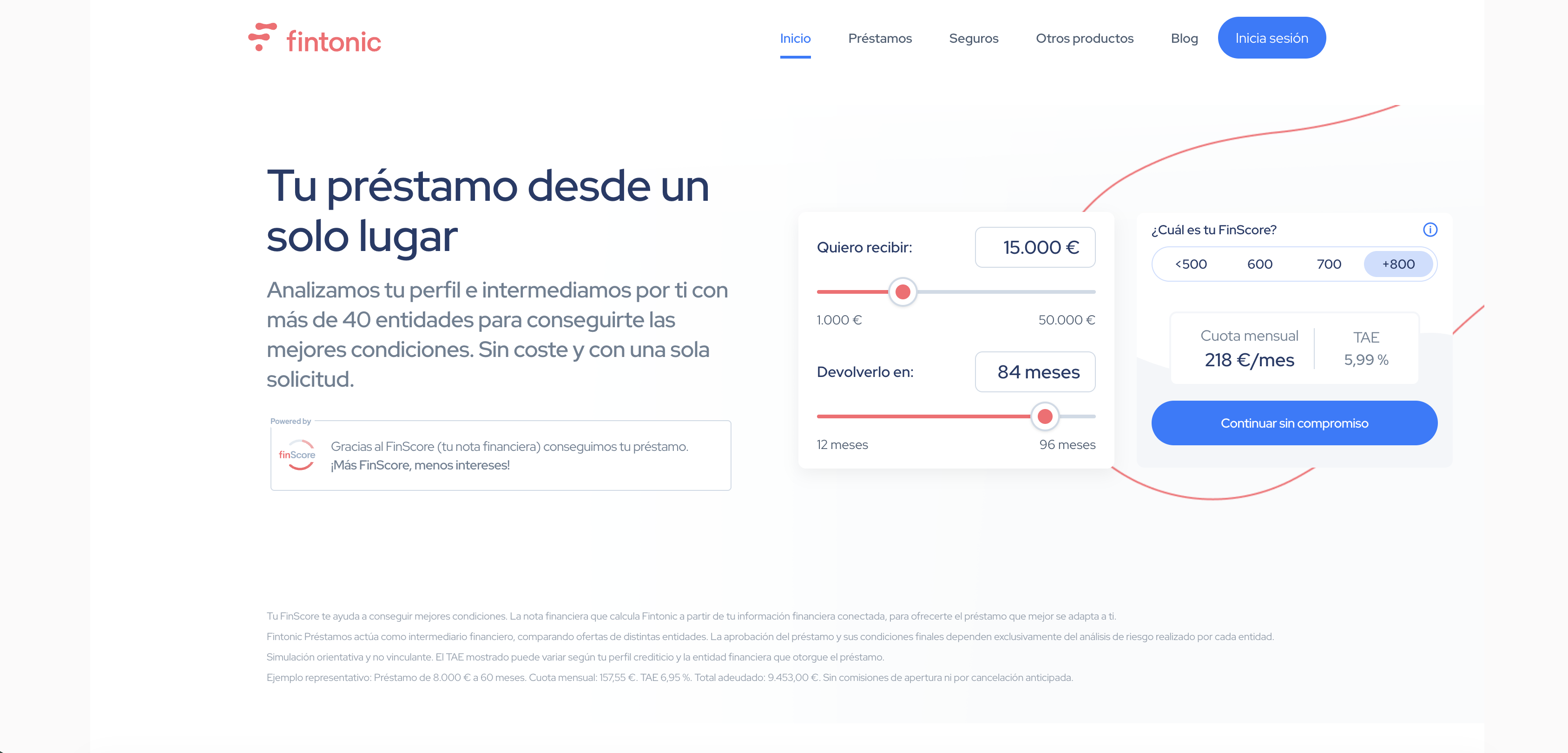

fintonic.com

Fintonic

fintonic.com🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Categories

Open BankingPersonal Finance

instantor.com

Instantor

instantor.com🇸🇪 Sweden

Open banking before open banking — that is essentially what Instantor was doing when it launched in 2010. Founded in Stockholm, the company built one of the early Nordic platforms for retrieving and analysing bank account data on behalf of lenders and financial services companies. Its technology gave lenders access to verified bank account information for credit scoring and identity verification — capability that PSD2 would later formalise into a regulated framework but that Instantor was providing under the screen-scraping and direct integration models of the pre-PSD2 era. The Nordic markets, with their high digital banking adoption and consumer comfort with sharing financial data, were a natural environment for the model to develop. Instantor was acquired by ClearScore in 2021, integrating its banking data infrastructure into one of the UK's largest credit comparison platforms. The acquisition reflected the consolidation pattern that has defined open banking infrastructure — early specialists building genuinely valuable technology and being absorbed by larger consumer-facing companies that need the underlying data capability. In the Nordic open banking landscape, Instantor was one of the foundational platforms whose technology continues to power credit decisions across multiple consumer fintech products even after its independent existence ended.

Categories

Open BankingLending

yapily.com

Yapily

yapily.com🇬🇧 United Kingdom

Yapily sits at the intersection of open banking and embedded finance, building the plumbing that lets fintech companies and enterprises tap into banking data and payments without reinventing the wheel. Founded in 2016, the London-based company operates as an API infrastructure layer—connecting to banks across Europe and beyond to unlock account information, payment initiation, and consent management at scale.

What makes Yapily different is how it abstracts away the complexity of working with hundreds of banks and their inconsistent technical standards. Rather than forcing developers to build individual integrations for each bank's API, Yapily provides a unified interface that normalizes everything. It's the translator between your app and the messy reality of legacy banking infrastructure.

The company operates in the B2B2C space, partnering with fintechs, neobanks, and enterprise software providers who need banking connectivity but lack the resources to build it themselves. Their customer base spans lending platforms, wealth apps, accounting software, and payment orchestration layers—essentially anyone whose product benefits from real-time access to customer bank accounts or the ability to initiate payments.

Yapily's positioning is deliberately unsexy: they're infrastructure, not consumer-facing. But that's precisely the point. In a landscape crowded with consumer fintechs chasing headlines, Yapily has built a quiet, profitable business serving the builders themselves. They're to open banking what Stripe is to payments—the backbone that lets innovation happen faster.

Categories

Embedded FinanceFinancial InfrastructureOpen Banking

currencycloud.com

Currency Cloud

currencycloud.com🇬🇧 United Kingdom

Currency Cloud powers cross-border payments for fintechs, banks, and platforms that move money internationally. Rather than building payment rails from scratch, companies plug into Currency Cloud's infrastructure to send, receive, and manage multi-currency transactions at scale. The platform handles the compliance complexity, FX pricing, and settlement logistics that make global payments so difficult.

What sets Currency Cloud apart is its positioning as the backbone rather than the front-end. While fintech darlings grab headlines with sleek consumer apps, Currency Cloud quietly powers payments behind the scenes for hundreds of financial services companies across Europe, Asia, and beyond. The company works with everyone from neobanks to traditional institutions to embedded finance platforms, letting them offer international payments without the headache of building their own infrastructure.

The European fintech scene has become increasingly reliant on infrastructure layers like this one—companies that solve the hard infrastructure problems so others can focus on customer experience and product innovation. Currency Cloud sits in that crucial middle tier, handling the pipes while others decorate the storefronts. It's a less visible kind of power, but arguably more fundamental to how modern fintech works.

Categories

Financial InfrastructurePaymentsOpen Banking

powens.com

Powens

powens.com🇫🇷 France

Powens sits at the intersection of open banking and financial data aggregation, helping European fintechs and traditional banks make sense of the fragmented payment and account landscape. Rather than building another me-too aggregator, the company positions itself as the connective tissue between institutions and the data they need to move capital efficiently and securely. Their platform ingests transaction data, payment initiation flows, and account information from thousands of financial institutions across Europe, surfacing clean, standardized intelligence to power lending decisions, fraud detection, and embedded finance experiences. What sets Powens apart is its focus on the continental European market—where open banking adoption is uneven and legacy banking infrastructure still dominates. While UK and US aggregators have enjoyed first-mover advantage, Powens saw an opportunity to build native expertise in Germany, France, Spain, and Benelux, where regulatory tailwinds and fragmented banking systems created genuine demand. The company works with both consumer-facing fintechs and institutional clients, meaning they've learned to navigate the messy reality of building infrastructure that talks to both sleek fintech apps and stuffy corporate banking platforms. This dual-sided approach has become their competitive moat—they understand both the user experience expectations of modern fintech and the compliance complexity of traditional finance. In the broader European fintech stack, Powens functions as a critical middleware layer, solving the unglamorous but essential problem of data connectivity that powers everything downstream—from embedded lending to fraud prevention to wealth management.

Categories

Fraud & SecurityFinancial InfrastructureOpen BankingLending

token.io

Token

token.io🇬🇧 United Kingdom

Token is a London-based open banking platform that sits at the intersection of infrastructure and consumer experience, making API-driven financial connectivity feel less like plumbing and more like a natural part of how money moves. Rather than asking users to log into their banks manually or hand over passwords, Token handles account aggregation and payment initiation through direct bank connections—the infrastructure most fintech apps and traditional banks should have built themselves but didn't.

The company's core insight is that open banking is only useful if it actually works across borders, across device types, and across the chaos of fragmented financial systems. Token's platform standardizes this mess, letting fintechs, banks, and payment companies offer seamless experiences without getting bogged down in regional variations or legacy bank APIs that still feel like they were written in 2003.

What sets Token apart in the European market is its focus on developer experience without sacrificing enterprise-grade security and compliance. While competitors offer raw API access or clunky consent flows, Token treats the entire interaction—from user authentication to transaction confirmation—as a product problem, not just a technical one. They're essentially the connective tissue that lets modern financial products actually work at scale.

Token's role in fintech infrastructure means it powers an invisible layer: the moment you authorize a payment or link an account in an app that "just works," Token's orchestration is likely running underneath. That's the kind of foundational utility the ecosystem desperately needs.

Categories

Financial InfrastructureDigital BankingOpen Banking

nordigen.com

Nordigen

nordigen.com🇱🇻 Latvia

Open banking infrastructure across Europe has been built by a small number of companies that compete on connectivity coverage, data quality, and pricing — and the cost dimension matters more than most observers initially appreciate. Nordigen was founded in Riga in 2016 with a thesis that open banking should be free at the basic level, with monetisation coming from value-added services rather than per-call API pricing. The free-tier offering changed the economics of building open banking products for European fintechs and developers, removing the cost barrier that had made experimentation expensive. Nordigen's platform covered banks across European markets through PSD2-compliant connectivity, providing account aggregation and payment initiation services. The company was acquired by GoCardless in 2022, integrating its open banking infrastructure into one of the largest European bank payment platforms. The acquisition reflects the consolidation pattern in European open banking — the standalone infrastructure businesses being absorbed into larger payment or banking groups that need the connectivity capability. In the European open banking landscape, Nordigen's free-tier model created competitive pressure that benefited the broader developer ecosystem, even after its independent existence ended through the GoCardless acquisition.

Categories

Financial InfrastructureOpen Banking

openwrks.com

OpenWrks

openwrks.com🇬🇧 United Kingdom

Credit decisions have historically been made on backward-looking data — credit files that reflect what happened years ago rather than what a person's financial life looks like today. OpenWrks was founded in London in 2017 to change that with open banking data. Its platform uses transaction data from bank accounts to generate real-time financial insights — income verification, affordability assessments, and cash flow analytics — that lenders, debt advisors, and financial services companies can use to make better decisions about the people they serve. The focus on affordability and debt support is deliberate — OpenWrks has built particular depth in the debt advice sector, providing tools that help debt charities and money guidance services understand their clients' financial situations with precision and speed that paper-based assessments cannot match. Its work with the Money and Pensions Service and other UK debt support organisations reflects a commitment to using open banking data for financial inclusion rather than purely commercial lending optimisation. In the open banking ecosystem, where most data applications focus on acquisition and credit origination, OpenWrks' orientation toward debt support and financial wellbeing is a distinctive positioning that has built genuine trust with the organisations that serve financially vulnerable people.

Categories

RegTechOpen Banking

yodlee.com

Yodlee

yodlee.com🇩🇪 Germany

Yodlee sits at the intersection of consumer financial data and the platforms that depend on it. Since the early 2000s, it's been quietly aggregating transaction history and account information across tens of thousands of financial institutions worldwide—the kind of unglamorous but essential infrastructure that powers everything from personal finance apps to enterprise banking systems. The company has evolved from a pure data aggregator into something more architecturally ambitious: a full-stack fintech operating system that connects consumers, their financial data, and the financial institutions and fintechs that need access to it.

The core proposition remains unchanged: connect to your bank, credit card, or investment account once, and Yodlee's network knows what you own, what you owe, and where your money flows. But the modern Yodlee is less about being a consumer brand and more about being the invisible backbone. It powers embedded finance experiences, drives decisioning for lenders who need to verify income or assess creditworthiness in real time, and provides the data layer that newer fintech competitors rely on to compete with legacy banks.

What separates Yodlee from point-solution competitors is its scale and exhaustiveness. Coverage matters in financial data aggregation—the difference between 95 percent and 99 percent institutional reach is the difference between a useful tool and a platform financial institutions trust. Yodlee operates at the latter level, serving banks, insurers, wealth managers, and a constellation of fintech challengers across North America, Europe, and Asia-Pacific.

In a crowded landscape of open banking APIs and PSD2-enabled competitors, Yodlee remains relevant because financial data aggregation remains hard at scale. It's the kind of infrastructure business that rarely makes headlines but never really goes out of fashion.

Categories

Financial InfrastructureIdentity & KYCOpen Banking