Country

Companies10 of 42

artemundi.com

Artemundi

artemundi.com🇩🇪 Germany

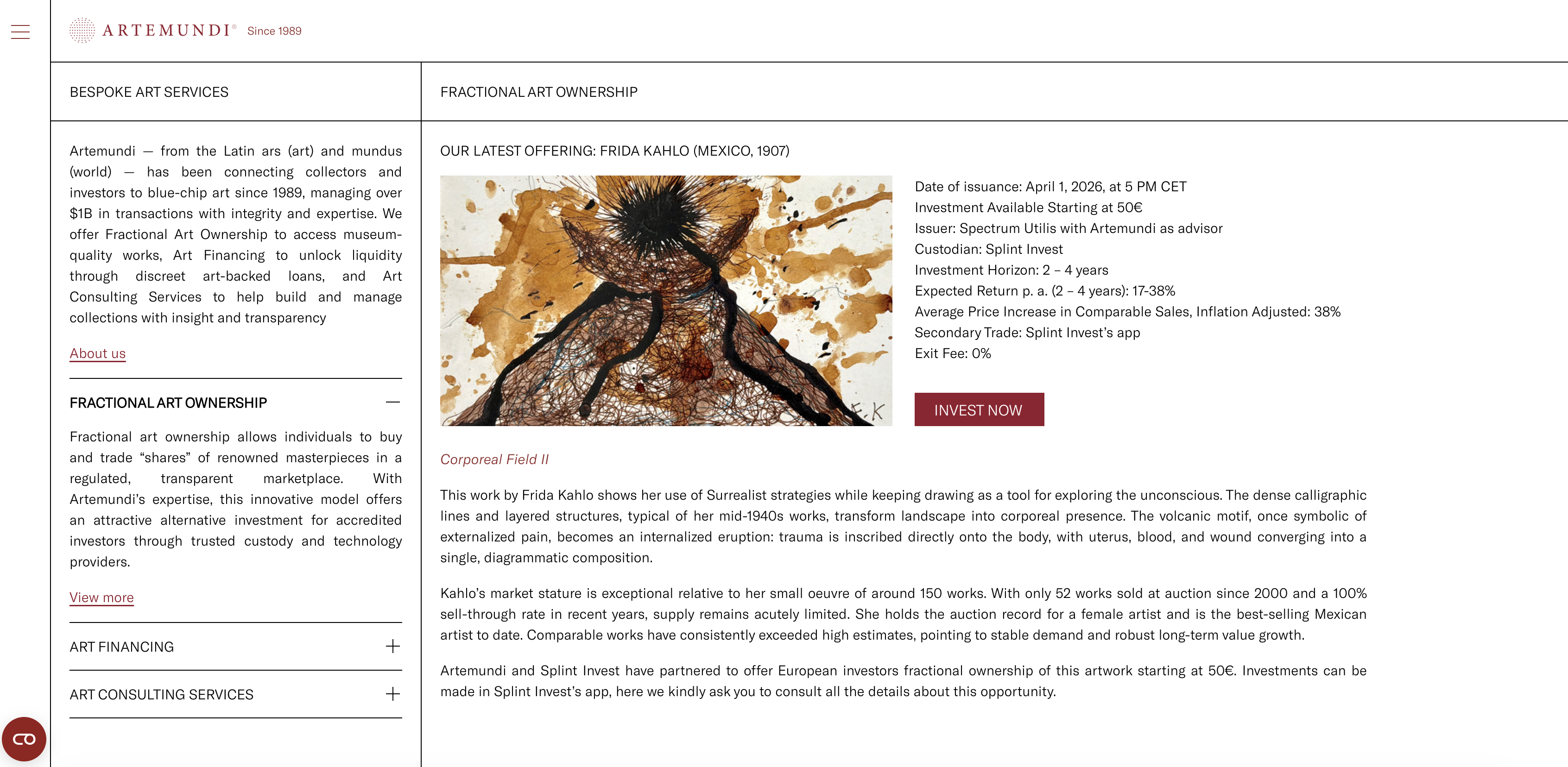

Artemundi is an alternative asset manager built for the modern wealth ecosystem. Rather than chasing traditional markets, the firm specializes in emerging market debt, private equity, and distressed assets—seeking returns where conventional investors see opacity. It's positioned at the intersection of hedge fund sophistication and institutional rigor, attracting wealth managers and sophisticated investors who understand that real returns often live outside the mainstream.

The company runs multiple investment vehicles targeting different risk appetites and timeframes, each managed with the discipline of a tier-one institutional shop. Their approach combines deep emerging market expertise with operational rigor, allowing them to navigate complexity that smaller competitors cannot. This isn't retail wealth management repackaged; it's institutional-grade alternative investing for those who can access it.

In the European wealth tech landscape, Artemundi represents the alternative asset class gatekeepers—firms that manage substantial capital across non-traditional strategies. While the fintech world obsesses over fractional shares and gamified trading, Artemundi operates in the space where serious capital allocation happens. They cater to family offices, pension funds, and institutional investors who view alternative assets as core portfolio components rather than exotic bets.

The firm embodies a particular European investment philosophy: skepticism of index-heavy approaches, appetite for frontier markets, and belief that skilled managers can exploit inefficiencies where passive strategies cannot. In an era of wealth fragmentation and advisor tech disruption, Artemundi remains a destination for institutional-grade alternative returns.

Categories

Wealth

c24.de

C24

c24.de🇩🇪 Germany

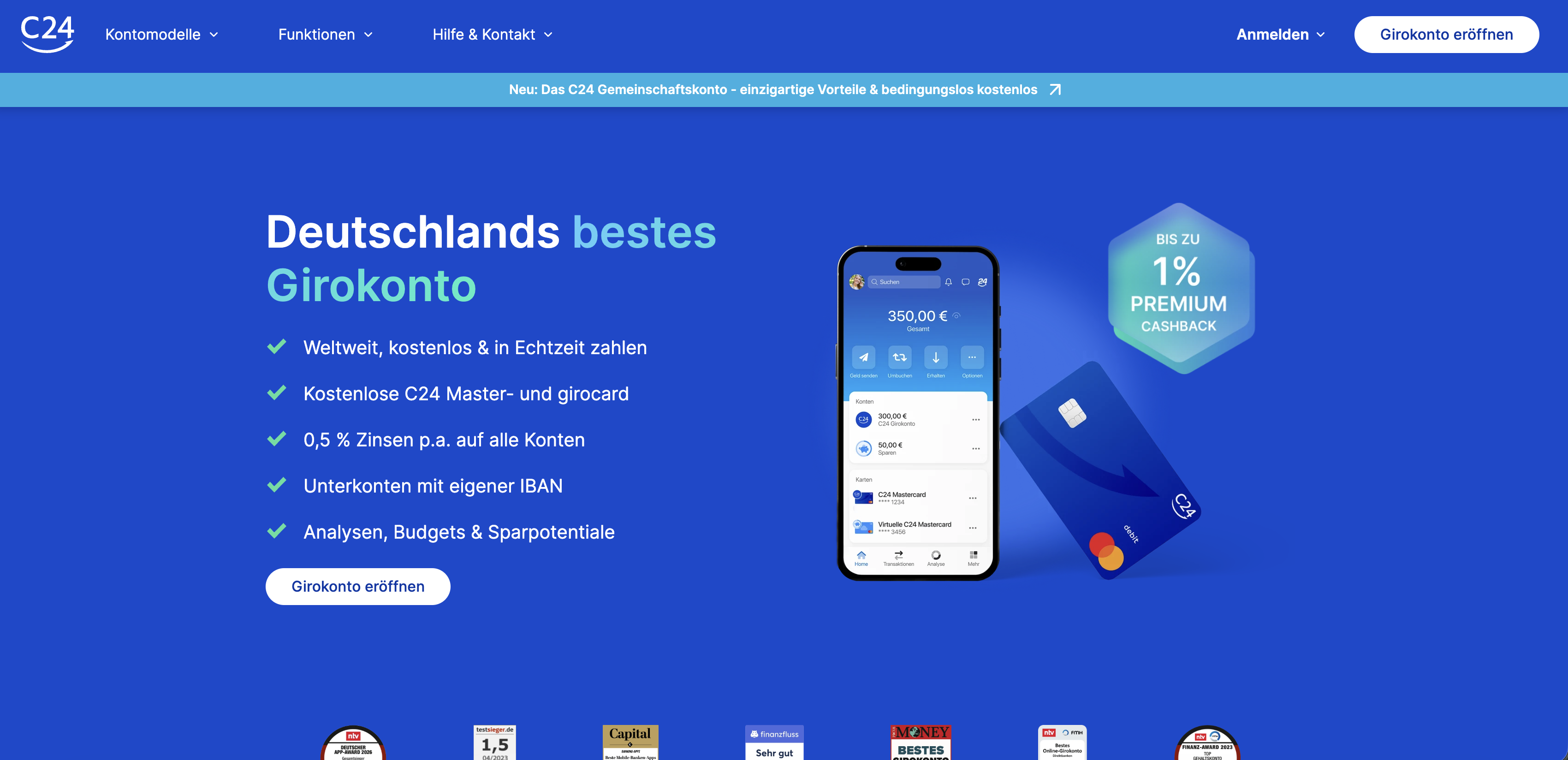

C24 is a Berlin-based mortgage platform that has quietly become one of Germany's fastest-growing digital real estate lenders. Rather than reinventing the entire mortgage process, C24 did something smarter: it took the bureaucratic nightmare of getting a home loan and compressed it into an app. You can apply, get a decision, and lock in rates without ever visiting a bank branch or talking to a loan officer.

The platform combines AI-powered underwriting with human expertise, delivering mortgage approvals in days instead of weeks. Borrowers upload documents once, answer questions about their property and finances through an intuitive interface, and receive personalized offers that compare across multiple lenders. The whole experience feels less like visiting a German bank and more like ordering something online.

In a market traditionally dominated by relationship banking and paperwork, C24 stands out by making mortgages transparent and competitive. German homebuyers, used to opaque pricing and slow processes, have embraced the speed and clarity. The company has grown into one of Central Europe's most recognized mortgage tech platforms, processing billions in loan volume annually.

C24 represents a broader shift in real estate finance: when you automate the friction, good execution becomes a competitive advantage. In Germany's conservative lending landscape, that's revolutionary.

Categories

Real Estate Finance

sumup.com

SumUp

sumup.com🇩🇪 Germany

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months.

The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager.

What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore.

SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Categories

PaymentsDigital BankingFinancial InfrastructureSME Finance

omnius.com

Omnius

omnius.com🇩🇪 Germany

Omnius is a European fintech infrastructure player that builds the plumbing for digital finance. Rather than launching consumer apps or chasing trends, the company focuses on giving financial institutions and fintech operators the core technology to move faster. The platform handles payment processing, account management, and the underlying APIs that let banks and non-banks operate at scale without reinventing the wheel.

What distinguishes Omnius in a crowded infrastructure market is its pragmatic approach to complexity. European banks still manage legacy core systems alongside new digital channels—a messy, expensive reality most fintech companies ignore. Omnius doesn't fight that; it sits in the middle, connecting old and new, and abstracts the chaos away from the business logic above it.

The company targets institutions that need to modernize faster than their technology stacks allow. That includes challenger banks that need banking-as-a-service foundations, traditional banks building new digital channels, and fintech companies that want to scale without owning every layer. It's unsexy infrastructure work—the kind that doesn't generate headlines but quietly powers the financial services layer that consumers interact with.

In the European fintech stack, Omnius occupies a critical but overlooked position: the vendor that lets faster companies stay fast, and slower ones move at all.

Categories

Financial InfrastructurePayments

auxmoney.com

auxmoney

auxmoney.com🇩🇪 Germany

auxmoney sits at the intersection of peer-to-peer lending and digital financial inclusion. The Berlin-based platform connects individual investors with borrowers seeking personal loans, sidestepping traditional bank gatekeeping through algorithmic credit assessment and a streamlined approval process.

Since 2007, it has built one of Europe's more mature alternative lending marketplaces, processing billions in credit and establishing itself as a credible counterweight to institutional finance for everyday lending needs. What sets auxmoney apart in the crowded P2P lending space is its focus on accessibility: borrowers who might struggle with conventional bank criteria can access capital, while investors gain exposure to diversified consumer credit without the friction of direct lending management. The platform automates origination, servicing, and investor payouts, handling the operational complexity that keeps most people out of direct lending. auxmoney doesn't pretend to be a bank—it's unapologetically a marketplace, transparent about risk and returns in ways traditional lenders rarely are.

In a European fintech landscape increasingly dominated by neobanks and payment startups, auxmoney represents a quieter but steadier category: the infrastructure that lets capital find borrowers efficiently. Its longevity and scale demonstrate that P2P lending, despite early hype and inevitable casualties, has become infrastructure for people and investors outside the conventional banking circle.

Categories

Lending

scalable.capital

Scalable Capital

scalable.capital🇩🇪 Germany

Scalable Capital sits at the intersection of wealth management and technology, offering algorithmic portfolio management that strips away the pretense of traditional advisory. The Berlin-based platform automates investment decisions through factor-based strategies, letting users build diversified portfolios without the six-figure minimums or quarterly check-ins that characterize private banking.

What makes Scalable different is its obsession with cost transparency. Rather than burying fees in percentages most investors never question, the platform charges a flat monthly fee regardless of account size, eliminating the perverse incentive for advisors to push larger positions. The investment thesis itself is refreshingly unsentimental: diversify broadly across global equities and bonds, rebalance automatically, and let compound interest do the work.

Scalable operates in a market crowded with robo-advisors, but it's positioned itself as the thinking person's alternative to both passive ETF apps and expensive human advisors. It's gained meaningful traction across Germany, Austria, and Switzerland, where wealth management has traditionally meant stuffy bank meetings and outdated fee structures.

The company represents a broader European fintech trend: taking institutional investment practices and making them accessible, affordable, and friction-free for ordinary people who simply want their money to work without constant hand-holding.

Categories

WealthPersonal Finance

exporo.de

Exporo

exporo.de🇩🇪 Germany

Exporo democratizes real estate investment in Europe by letting regular investors back commercial property projects with surprisingly small cheques. Instead of needing six figures and a relationship manager, you can pledge €500 towards a Berlin office building or Hamburg retail space and earn returns as the project completes. The platform essentially crowdfunds property deals across Germany, Austria, and Switzerland, handling the legal complexity and underwriting legwork while keeping investors in the loop through transparent updates and quarterly reports.

What sets Exporo apart is its focus on institutional-quality real estate rather than speculative ventures. Projects are vetted by in-house analysts, and the company retains skin in the game by co-investing on deals it underwrites. The platform appeals to people frustrated with negative interest rates at traditional banks—here you're earning 4–7% returns tied to actual brick-and-mortar assets rather than betting on stock price appreciation.

In a landscape crowded with retail investment apps and crypto-enabled speculation, Exporo occupies a distinctly European middle ground: serious about underwriting standards, transparent about risk, and aligned with the slow-moving rhythms of real property finance rather than algorithmic trading. It's become the go-to platform for German-speaking investors seeking alternative yields without moving into illiquid private equity.

Categories

Real Estate Finance

hellogetsafe.com

Getsafe

hellogetsafe.com🇩🇪 Germany

Getsafe is building insurance for the digital age, stripping away the complexity and paperwork that make traditional coverage feel like a relic. Founded on the premise that buying insurance shouldn't require a PhD in fine print, the Berlin-based insurtech has made it possible to buy, manage, and claim on policies entirely through a smartphone app. The company doesn't issue policies itself—it partners with licensed insurers—but it's reimagined every touchpoint of the experience, from onboarding (minutes, not hours) to claims (AI-powered and often resolved instantly). Where legacy insurers still operate like bureaucracies, Getsafe feels like a consumer product.

The startup has quietly built a loyal user base across Germany, France, Spain, and Austria by targeting younger, digitally-native consumers who would rather avoid call centres altogether. Its approach is deliberately inclusive: pricing is transparent, policies are customizable, and the app handles everything from renewal reminders to claims documentation in a friction-free way. Unlike traditional insurance companies that treat digital as an afterthought, Getsafe is built digital-first from the ground up. The company generates revenue through commission-based partnerships with insurers and through incremental service fees.

In a category historically dominated by incumbents and tied to physical distribution, Getsafe represents a quiet but meaningful shift toward consumer-centric insurance platforms. It's not disrupting the regulatory infrastructure of insurance, but it's successfully disrupting how people interact with it—proving that a better app can win even in one of Europe's most conservative financial sectors.

Categories

InsurTech

clark.de

Clark

clark.de🇩🇪 Germany

Clark is disrupting the messy business of insurance administration in Germany, Austria, and Switzerland by giving customers a single digital interface to manage all their policies—regardless of which insurer they're with. Rather than forcing people to juggle multiple providers and renewal notices, Clark aggregates everything into one place and handles the administrative grunt work: comparing coverage, finding better deals, and switching policies when it makes sense.

The app has become the go-to way for tens of thousands of Europeans to actually understand what they're paying for and stop overpaying. What sets Clark apart is that it doesn't just manage policies after you buy them—it actively renegotiates on your behalf, leveraging collective bargaining power to find cheaper rates across competitors. You authorize the switch, Clark handles the paperwork. Most insurance platforms either sell you products or help you compare; Clark does neither. Instead, it sits between you and the entire market, keeping your interests first and taking a commission only when it saves you money. The company has essentially made insurance administration feel like it's from the 2020s rather than the 1990s. For millions of Europeans stuck with scattered policies, outdated coverage, and premium shock every renewal cycle, Clark has become infrastructure.

Categories

InsurTech

solarisgroup.com

Solaris

solarisgroup.com🇩🇪 Germany

Solaris is a Berlin-based fintech infrastructure platform that lets financial institutions and fintechs launch their own digital banking products without building tech from scratch. Rather than wrestling with legacy core banking systems, clients plug into Solaris's cloud-native API layer to issue cards, manage accounts, and process payments at speed.

The company operates in the shadows of most consumer apps—you won't see the Solaris logo in an app store—but its backbone runs through dozens of European fintechs, neobanks, and traditional financial institutions. Think of it as the plumbing that powers other people's banking ambitions.

Solaris dominates a specific niche: the BaaS (Banking-as-a-Service) and embedded finance layer for Europe. While competitors like Thought Machine and Temenos chase enterprise banking overhauls, Solaris stays focused on the modern fintech workflow. Its modular design appeals to companies that need speed and flexibility, not a 10-year implementation project.

In a market crowded with infrastructure plays, Solaris has become essential plumbing for European digital banking. It sits at the intersection of regulatory compliance, technical simplicity, and startup ambition—precisely where the next wave of European fintech is being built.

Categories

Financial InfrastructureDigital BankingPayments