Country

Companies9 of 9

nexi.it

Nexi

nexi.it🇮🇹 Italy

Nexi is Italy's largest payment services operator, controlling the infrastructure that moves money across the country's retail and corporate sectors. Founded in 2013 through a merger of two major Italian payment processors, it manages card transactions, merchant acquiring, and digital payment rails for banks, retailers, and businesses across Europe.

The company operates across the full payments stack—from traditional POS terminals and card networks to modern API-based solutions and instant payment systems. Unlike most fintech startups, Nexi doesn't target consumers directly. Instead, it powers the payment backbone for Italian and European financial institutions and retailers, processing tens of billions in transactions annually. Its business model sits at the intersection of traditional payment infrastructure and modern open banking, positioning it as a critical node in Europe's shift toward real-time payments and embedded finance.

Nexi's role is unglamorous but essential: it's the plumbing that makes modern commerce work, handling everything from contactless cards to mobile wallets to cross-border transfers. In the broader European fintech landscape, it represents the "boring" but profitable core—the infrastructure layer that fintechs themselves depend on to function.

Categories

PaymentsFinancial InfrastructureOpen Banking

satispay.com

Satispay

satispay.com🇮🇹 Italy

Satispay cuts through the noise of payment processing by letting consumers pay directly from their bank account at checkout, skipping cards entirely. It's a mobile-first payment solution that arrived in Europe when digital wallets were becoming ubiquitous, but with a twist: it works offline and without requiring consumers to pre-load funds or enter card details repeatedly.

The company operates across Italy, France, Belgium, and other European markets, positioning itself as a bridge between traditional banking and modern commerce. Rather than competing head-to-head with card networks, Satispay enables merchants to accept payments through a lightweight app integration, with consumers confirming transactions via their phones in seconds.

What sets Satispay apart is its focus on simplicity and lower merchant costs compared to card acquiring. While payment gateways obsess over feature parity with every major card scheme, Satispay keeps the experience minimal: scan, tap, pay. It appeals to retailers tired of high interchange fees and consumers who prefer direct bank debits over recurring card charges.

In a fragmented European payments landscape, Satispay represents a pragmatic alternative to cards for in-store and online commerce, carving out space by solving a specific friction point rather than trying to be everything.

Categories

Embedded FinancePayments

scalapay.com

Scalapay

scalapay.com🇮🇹 Italy

Scalapay is a BNPL (buy now, pay later) platform built for the European e-commerce market, offering shoppers the ability to split purchases into interest-free instalments at checkout. Rather than simply bolting financing onto existing payment flows, Scalapay positions itself as a full-stack infrastructure play—handling underwriting, risk management, and merchant integration from a single API. The company targets mid-market and enterprise retailers across fashion, electronics, and beauty verticals, regions where instalment purchasing is becoming table stakes for conversion.

What sets Scalapay apart is its focus on merchant flexibility and real-time decision-making. While competitors often impose rigid lending terms or lengthy approval processes, Scalapay emphasizes transparent pricing and instant qualification, allowing merchants to offer financing without friction or hidden costs. The platform integrates seamlessly into checkout experiences—both web and mobile—and provides merchants with detailed analytics on customer behaviour and financing uptake.

Scalapay operates in a crowded BNPL landscape, but differentiates through its emphasis on profitability and sustainable lending rather than growth-at-any-cost customer acquisition. The company has expanded across multiple European markets, particularly in Southern Europe and the Mediterranean, where instalment culture is deeply embedded. Its positioning sits between pure-play consumer lenders and white-label infrastructure providers, serving merchants who want financing capabilities without building their own credit infrastructure.

In the broader fintech ecosystem, Scalapay exemplifies the maturation of embedded finance—moving beyond the novelty of BNPL into building durable, profitable lending platforms that merchants and consumers both trust.

Categories

Embedded FinancePaymentsBNPL

credimi.com

Credimi

credimi.com🇮🇹 Italy

Credimi sits at the intersection of e-commerce and embedded finance, solving a problem that online retailers have largely ignored: making checkout friction disappear. Rather than forcing customers to choose between card payments and bank transfers, Credimi lets shoppers access buy-now-pay-later directly at the point of sale, turning the checkout moment into a financing decision rather than a payment one. The company essentially white-labels installment lending for merchants, handling everything from credit decisioning to collections behind the scenes.

What sets Credimi apart in a crowded BNPL market is its focus on the merchant relationship rather than the consumer one. While competitors chase customer loyalty through branded apps and direct marketing, Credimi takes a B2B approach, embedding its credit engine into partner payment flows and e-commerce platforms. This means retailers get better conversion rates without bearing the customer acquisition cost. The company operates across multiple European markets, particularly strong in the Nordics and DACH region, where fintech-native commerce has matured fastest.

In an industry obsessed with speed and simplicity, Credimi's real edge is its underwriting—it deploys machine learning to make instant credit decisions without the awkward friction of traditional lending. This isn't flashy consumer fintech; it's infrastructure. But it's exactly what online retailers need to compete in markets where BNPL has become table stakes.

Categories

Embedded FinanceBNPL

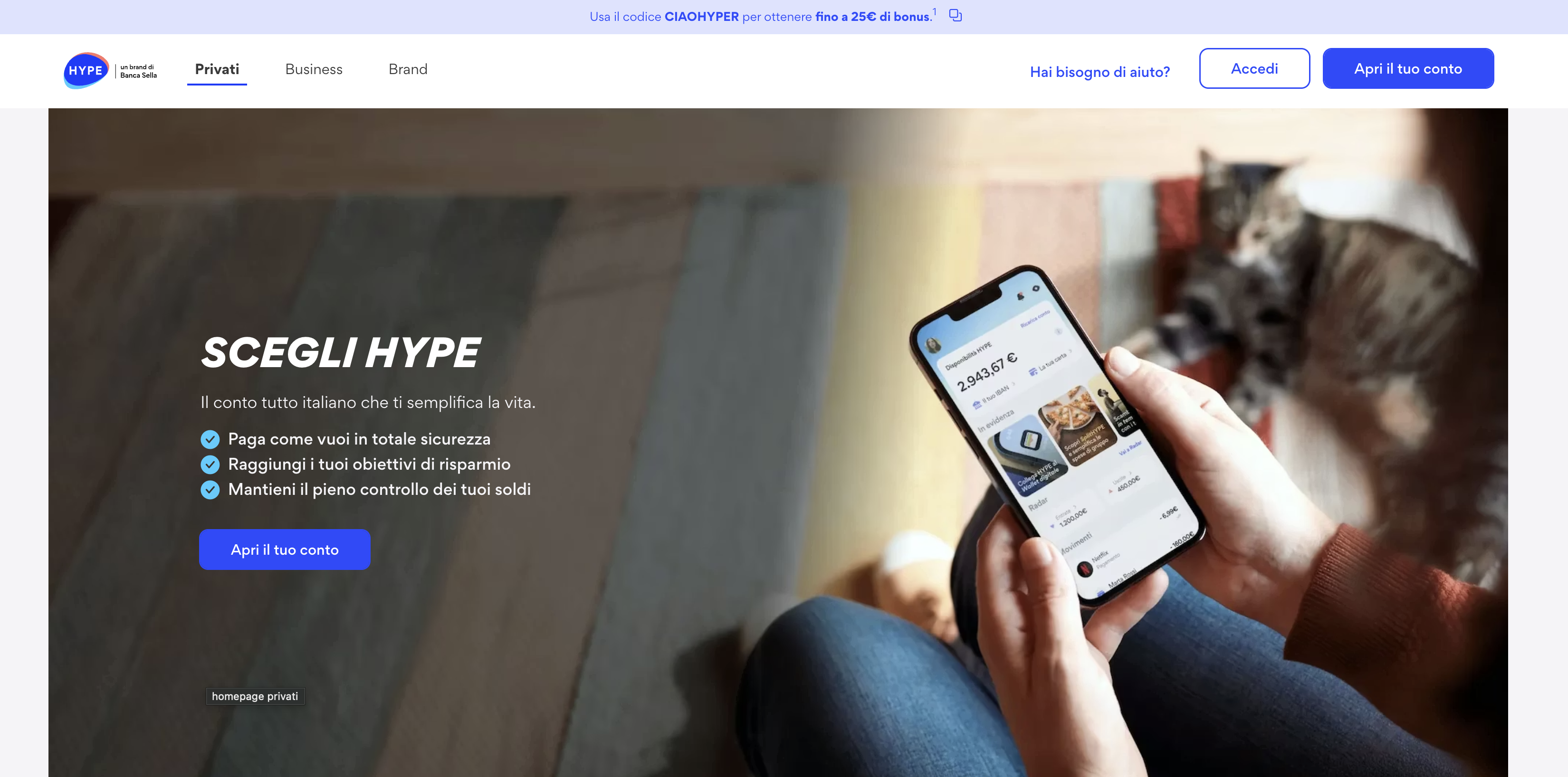

hype.it

Hype

hype.it🇮🇹 Italy

Hype is Italy's answer to the mobile banking revolution, a neobank that has spent nearly a decade proving that digital-first doesn't mean stripped-down. Rather than chase global scale with generic features, Hype has built a hyperlocal following by understanding what young Italians actually want from their money: instant transfers, cashback rewards, zero monthly fees, and a sleek app that doesn't feel like it was designed by a committee of compliance officers.

The platform operates as a digital-only current account backed by actual IBAN credentials, so it's not playing at banking—it's the real thing, licensed and regulated. Users get a contactless Mastercard, push-notification alerts for every transaction, and the kind of interface that makes traditional banking feel positively medieval by comparison. Hype's cashback ecosystem is its signature move, offering percentage returns on spending across partner merchants, which transforms the app from a mere account holder into a lifestyle spending companion.

In a market where European neobanks have largely converged around identical feature sets, Hype has chosen to go deep rather than broad, cementing itself as the default neobank for Italian millennials and Gen Z. It's proof that you don't need hundreds of millions in funding or ambitions to be present in every time zone to build something genuinely meaningful. The company represents a particular kind of fintech success: profitable, focused, and beloved by its core audience rather than chased by venture capitalists.

Hype demonstrates that the future of banking in Europe isn't about creating one global super-app, but rather a network of fiercely intelligent regional players, each optimized for the specific financial behaviors and preferences of their home market.

Categories

Digital BankingPersonal Finance

illimity.com

illimity

illimity.com🇮🇹 Italy

illimity is an Italian digital bank built from scratch for the modern era, refusing the bloat of legacy banking while maintaining the credibility of a proper banking license. The Milan-based lender makes its money by funding SMEs, distressed companies, and consumer credit—markets where traditional banks have largely checked out or moved at glacial speed. Unlike neobanks chasing retail deposits with app aesthetics, illimity operates as a genuine credit institution, meaning it takes deposits and extends loans at scale.

The bank's core insight is straightforward: the best businesses and borrowers often get rejected by automated systems or stuck in months-long approval queues. illimity cuts through that friction with data-driven underwriting and a willingness to look beyond standard credit scores. For SMEs, it offers working capital facilities, invoice finance, and acquisition financing. For consumers, it provides personal loans and mortgages. It also runs a dedicated division for acquired distressed loans and restructured credits—a niche most retail-focused fintechs have no interest in.

In the crowded Italian banking landscape, illimity stands apart by combining tech-first operations with genuine lending expertise. It's not pretending to be a bank; it actually is one. Where most European digital lenders hit a ceiling—they can't take deposits or originate real credit—illimity has built the full stack. Its positioning sits somewhere between a next-gen retail bank and a specialized credit platform, serving customers ignored or underserved by the incumbents.

Categories

Digital BankingLendingSME Finance

fabrick.com

Fabrick

fabrick.com🇮🇹 Italy

Fabrick operates in the unglamorous but essential corner of fintech where plumbing meets innovation. The Italian firm builds the digital infrastructure that lets banks, fintechs, and non-financial companies offer financial services without building everything from scratch. It's Banking-as-a-Service for a continent that still runs on legacy rails, but Fabrick is quietly rewiring how money moves across borders and between accounts.

The company offers a full stack of APIs and platforms covering payments, accounts, lending, and open banking connectivity. Rather than forcing clients into rigid templates, Fabrick positions itself as a modular toolbox: plug in what you need, leave out what you don't. This flexibility appeals to enterprises tired of one-size-fits-all solutions and startups wanting to launch financial products without the regulatory headache of building a bank license from scratch.

In a European fintech landscape dominated by consumer-facing rebels, Fabrick is the B2B backbone nobody talks about at conferences but everyone quietly depends on. It competes by being boring in all the right ways—reliable, compliant, and deep enough in the weeds to handle edge cases that make other platforms crumble. The company has steadily expanded across Europe, positioning itself as the infrastructure layer for a generation of embedded finance plays.

Categories

Embedded FinanceFinancial InfrastructurePaymentsOpen BankingLending

axerve.com

Axerve

axerve.com🇮🇹 Italy

Axerve is an Italian payment orchestration platform that handles the messy middle ground between merchants and the fragmented world of European payment networks. Rather than forcing businesses to build integrations with dozens of acquirers, processors, and alternative payment methods, Axerve sits between them—routing transactions intelligently, managing failures, and turning what should be simple into something actually manageable. The platform connects to over 200 payment methods across Europe, from traditional card networks to regional players and emerging wallets, all accessible through a single API. What sets Axerve apart in a crowded space is its focus on the European complexity that most global payment platforms gloss over. They understand that Italian merchants need different acquiring rules than German ones, that transaction regulations shift by country, and that real flexibility means handling local nuances without forcing businesses to hire armies of integration engineers. The company operates with the efficiency of fintech but the institutional credibility of a traditional payments company—they're backed by solid Italian financial infrastructure rather than pure venture capital. For mid-market and enterprise merchants navigating Europe's byzantine payments landscape, Axerve removes the integrations tax and lets teams focus on selling instead of managing payment plumbing. In the broader fintech ecosystem, Axerve represents the infrastructure layer that rarely gets press but quietly enables thousands of European businesses to accept payments without drowning in technical debt.

Categories

Financial InfrastructurePayments

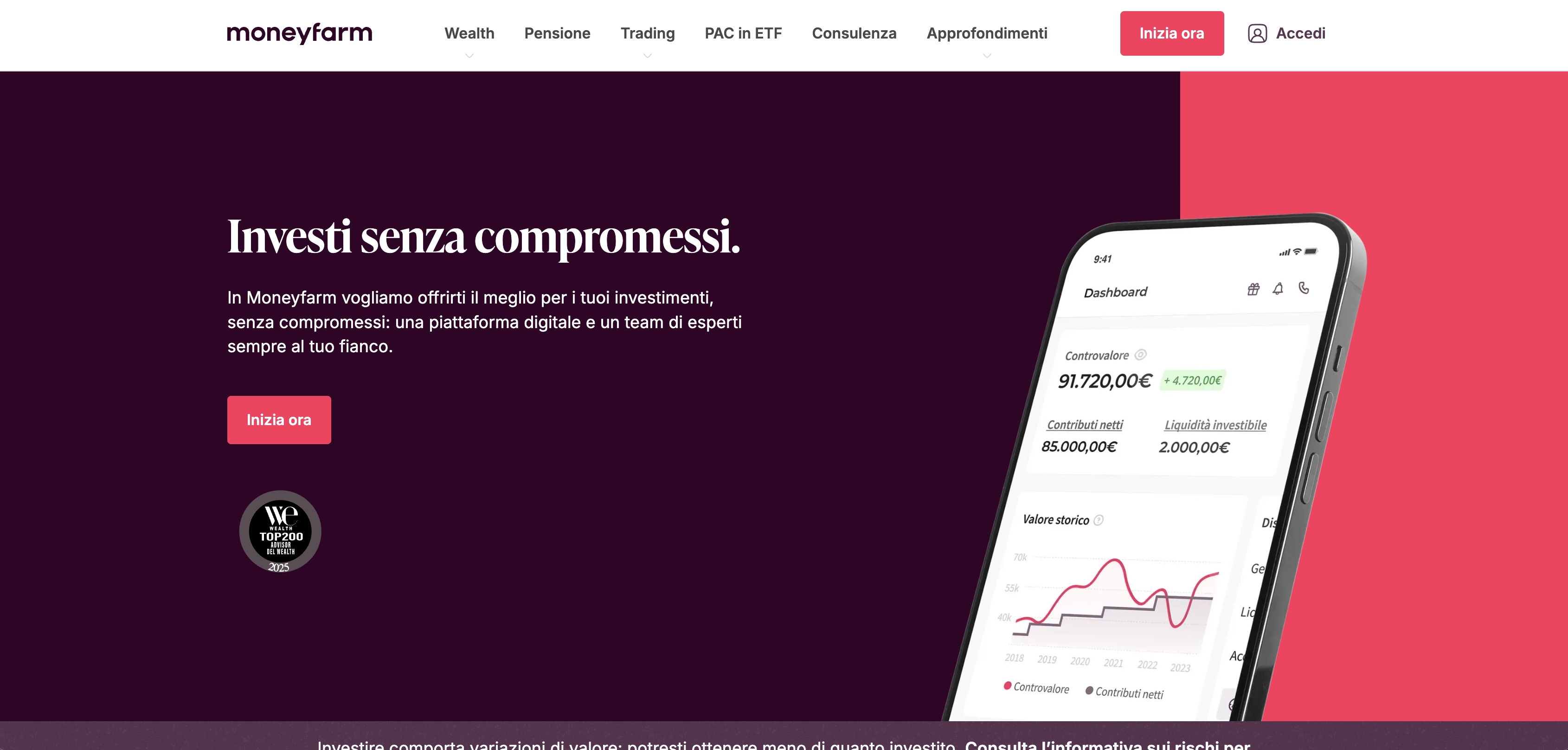

moneyfarm.it

Moneyfarm

moneyfarm.it🇮🇹 Italy

Robo-advisory in Italy faces the particular challenge of building investor confidence in a market where retail investment participation has historically been low and trust in financial institutions has been complicated by decades of banking sector difficulties. Moneyfarm was founded in Milan in 2011 and grew into one of the largest digital wealth managers in Europe by addressing that confidence problem directly — combining algorithmic portfolio management with human investment consultants who provide personalised guidance to clients who want it. The hybrid model differentiates it from pure robo-advisors that rely entirely on questionnaires and from traditional wealth managers that gatekeep advice behind high minimums. Moneyfarm has expanded across Italy, the UK, and Germany, building a substantial business in markets with very different investor cultures and regulatory environments. The company has attracted backing from major investors including Allianz Asset Management and Cabot Square Capital, reaching billions in assets under management. In the European wealth tech landscape, Moneyfarm represents one of the more successful examples of a digital wealth manager building genuinely cross-border scale rather than remaining confined to a single market — and its hybrid model of algorithmic management plus human advice has proven more durable than purely algorithmic approaches in markets where trust must be built more carefully.

Categories

WealthPersonal Finance