Country

Companies6 of 6

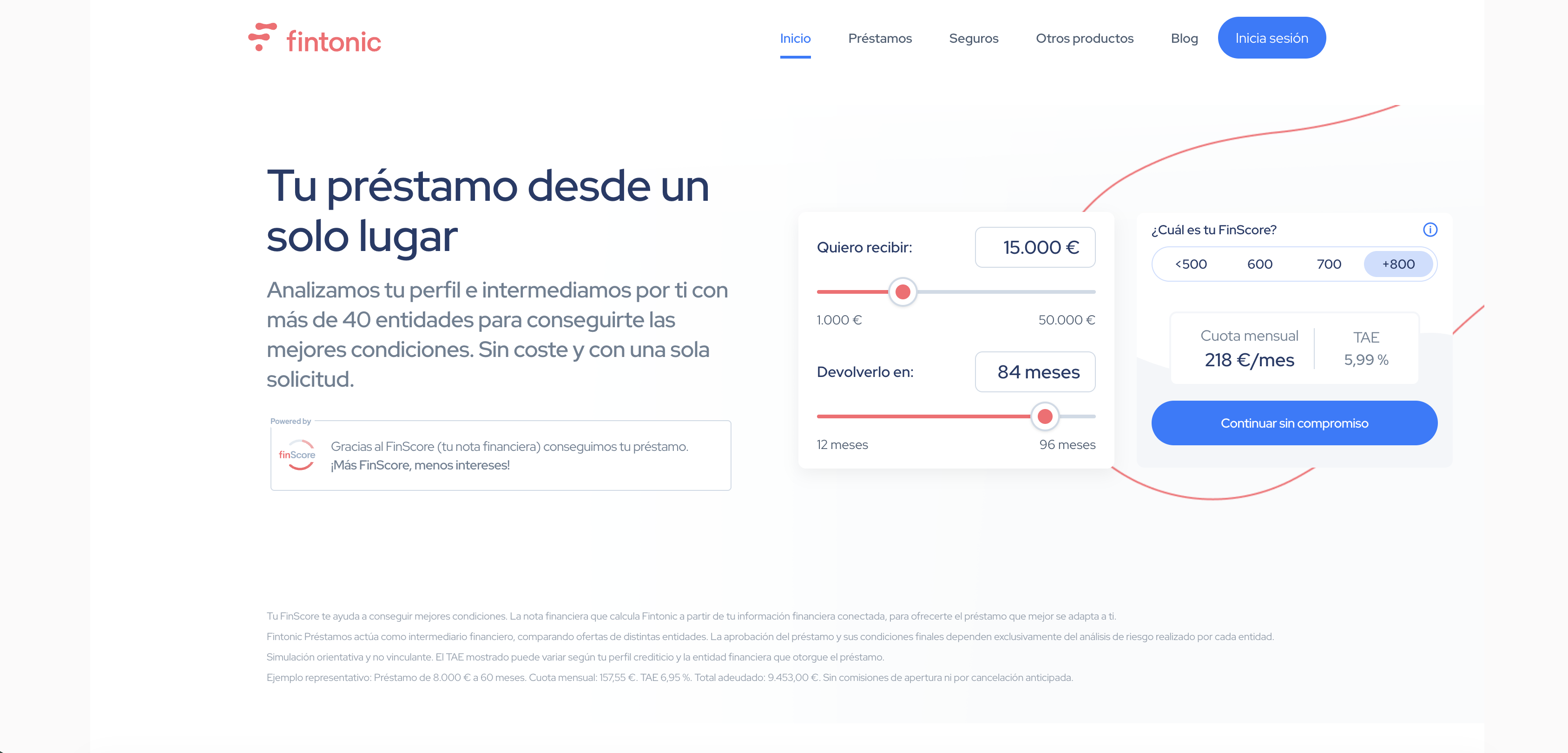

fintonic.com

Fintonic

fintonic.com🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Categories

Personal FinanceOpen Banking

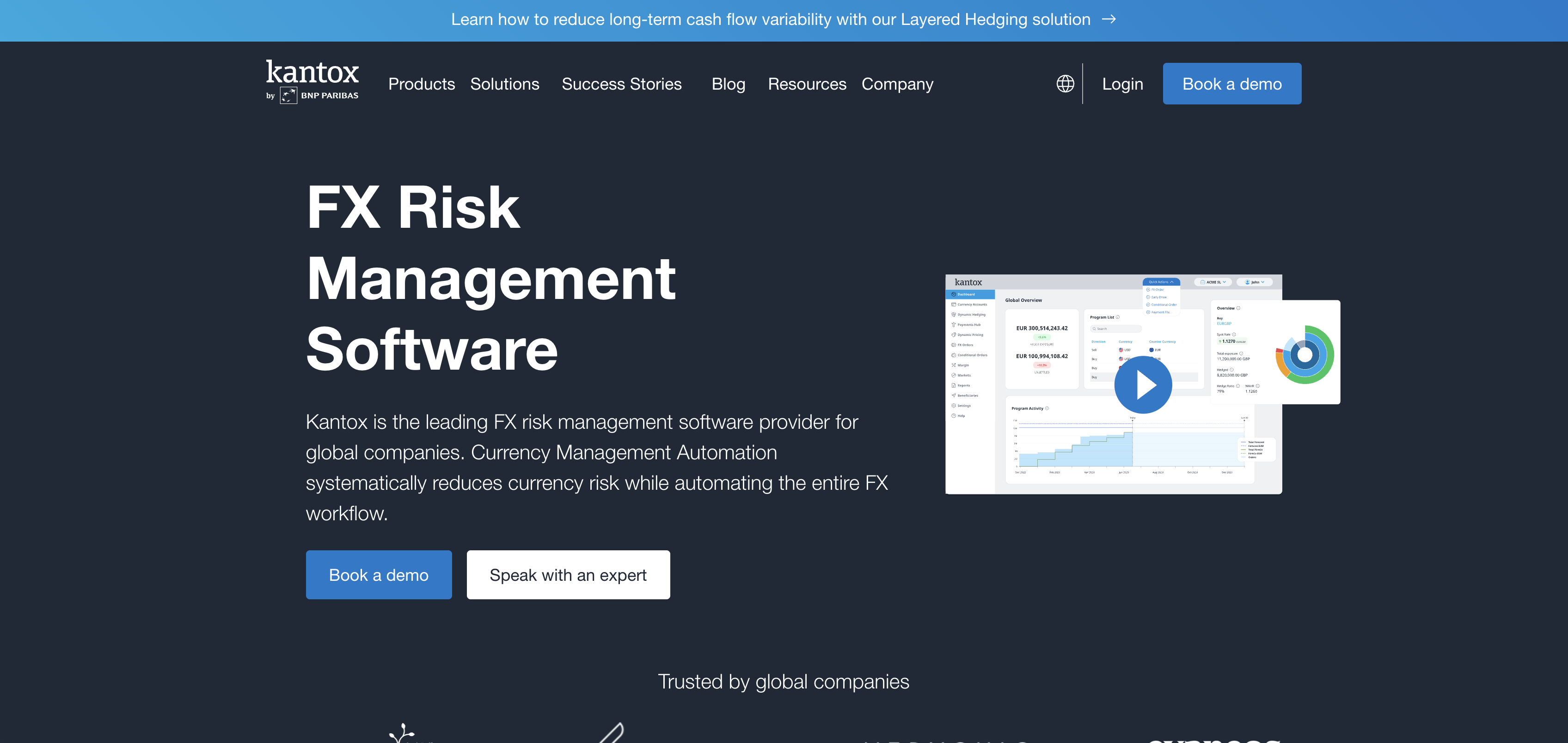

kantox.com

Kantox

kantox.com🇪🇸 Spain

Kantox sits at the intersection of corporate finance and fintech, solving a problem that has plagued treasurers and CFOs for decades: the cost and complexity of managing foreign exchange. Rather than forcing companies through the byzantine world of traditional banks or crude hedging tools, Kantox built a platform that lets businesses buy and sell currency with transparency, speed, and intelligence.

The platform aggregates liquidity from multiple sources—banks, non-bank liquidity providers, and peer matching—and surfaces the best rates in real time. No more vendor lock-in, no more opaque spreads, no more waiting. A mid-market company can execute a multi-million euro FX trade in minutes, seeing exactly what they're paying and why.

What sets Kantox apart in a crowded treasury tech space is its refusal to abstract away the mechanics. The platform shows you the market, then lets you trade. It's designed for finance professionals who know what they're doing and want control back from intermediaries. The company has built serious depth in emerging markets and supply chain currencies, which most legacy providers still treat as afterthoughts.

Kantox represents a broader shift in European fintech: the recognition that some of the most valuable problems live in the unglamorous corners of corporate finance, where even small improvements in execution cost save companies millions annually. In that sense, it's doing for FX what more visible fintechs have done for payments—stripping away friction and opacity from a process that should have been digital decades ago.

Categories

PaymentsTreasury

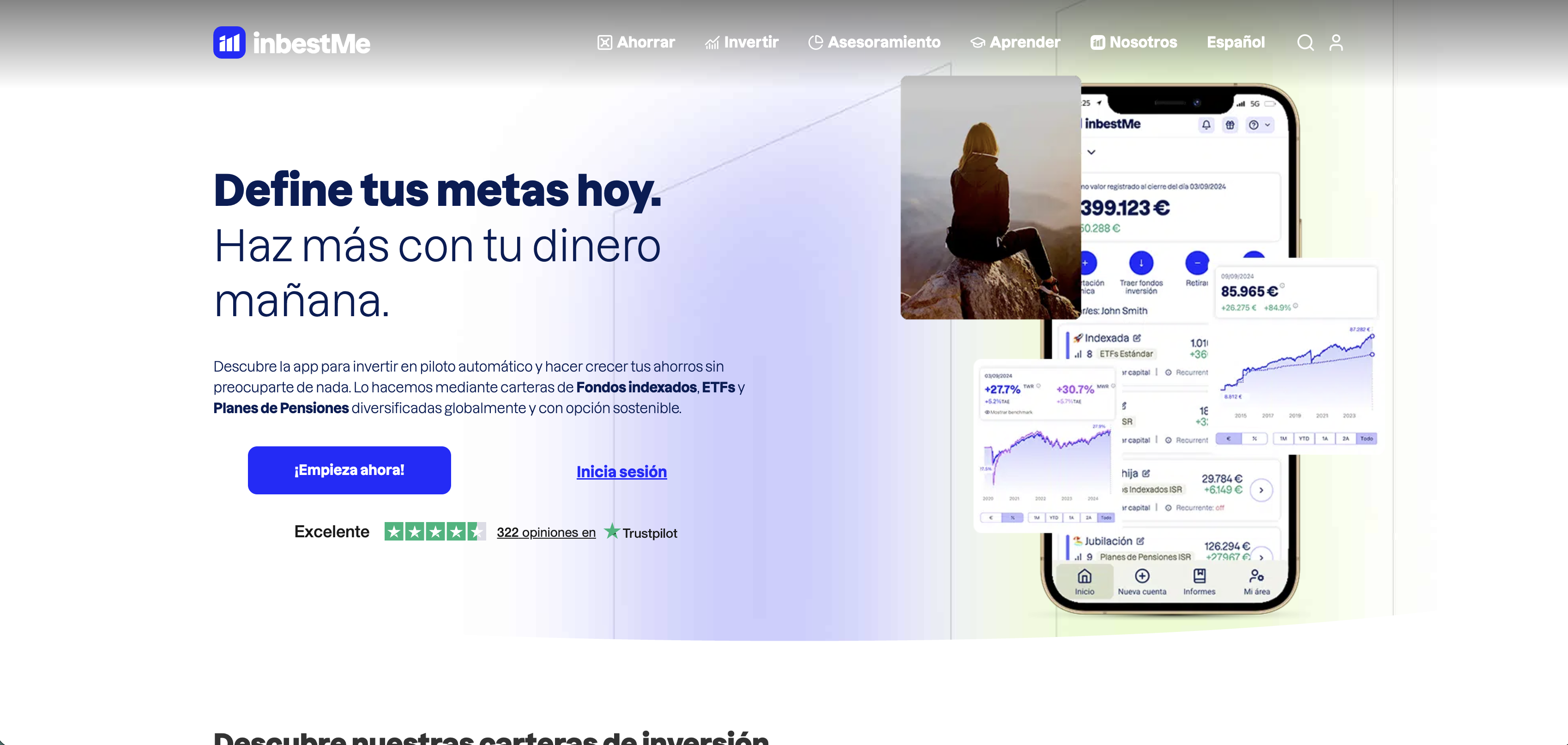

inbestme.com

inbestMe

inbestme.com🇪🇸 Spain

Spain's investment culture has traditionally been more conservative than other major European markets — a population with high savings rates but low investment participation, and a financial advisory landscape dominated by banks that have not always had their clients' interests at the centre of their advice. inbestMe was founded in Barcelona in 2014 to bring transparent, low-cost robo-advisory to the Spanish market. Its platform offers diversified ETF portfolios with multiple risk profiles and specialised strategies including socially responsible investing — a category that has resonated particularly with the Spanish retail investor segment that values investment products with clear values alignment. The company has built a position in the Spanish wealth tech market alongside Indexa Capital and Finizens, the three companies that have effectively defined Spanish robo-advisory. In the Iberian market, where Indexa has built its position on aggressive cost minimisation and Finizens on automated saving habits, inbestMe has differentiated through SRI portfolios and a broader range of investment strategies. In the European robo-advisory landscape, the Spanish market has emerged as one of the more competitive — proof that consumer demand for low-cost diversified investing exists wherever transparent products are made available, even in markets that financial institutions have written off as resistant to change.

Categories

WealthPersonal Finance

bnext.es

bnext

bnext.es🇪🇸 Spain

bnext is a Spanish neobank built for the self-employed and small business owners who've outgrown traditional banking but don't need enterprise complexity. It strips away the bloat of legacy banks and focuses on what actually matters: a mobile-first account, competitive forex rates, and transparent fees with no surprise charges. The platform handles invoicing, expense tracking, and basic bookkeeping alongside core banking, positioning itself as a unified workspace rather than just another digital bank. Where established institutions still treat SMEs as afterthoughts, bnext treats them as the primary customer. It's designed for the freelancer checking balances between client calls and the startup founder who wants one dashboard instead of five browser tabs. The company has carved out real traction in Spain and increasingly across Europe, proving there's genuine demand for banking that actually understands how modern small business works.

Categories

PaymentsDigital BankingSME Finance

kviku.com

Kviku

kviku.com🇪🇸 Spain

Instant credit at the point of need — a small loan approved in seconds, disbursed before the moment of purchase passes — is one of the more powerful applications of modern credit technology. Kviku was founded in 2013 and operates as a digital consumer lender offering virtual credit cards and instalment loans across multiple markets including Spain, Poland, Kazakhstan, and the Philippines. Its model is built around speed and accessibility: a fully automated underwriting process that makes credit decisions in real time using alternative data, targeting the segment of consumers who need small amounts quickly and are underserved by traditional credit products. The virtual credit card format is particularly relevant in markets where physical card infrastructure is less developed but smartphone penetration is high. Kviku operates across a wide geographic footprint for a company of its size, reflecting the scalability of a model that is fundamentally about credit technology rather than physical distribution. In the embedded finance and BNPL context, Kviku represents the direct lending end of the spectrum — not a buy now pay later product embedded in a merchant checkout, but a digital credit line that consumers carry with them to any point of purchase.

Categories

Lending

group.indexacapital.com

Indexa Capital

group.indexacapital.com🇪🇸 Spain

Indexa Capital is a robo-advisor built for European investors who want algorithmic portfolio management without the pretense or premium pricing of traditional wealth advisors. The Madrid-based firm automates asset allocation and rebalancing across a diversified basket of low-cost ETFs, letting retail investors access institutional-grade portfolio construction at a fraction of the cost of human advisors.

The platform handles everything from onboarding through ongoing portfolio optimization, using rules-based algorithms to maintain target allocations and harvest tax losses. It's designed for the investor who understands that beating the market consistently is a fool's errand, and who'd rather pay a flat or AUM-based fee to stay the course than chase alpha with a human advisor.

Indexa operates across Spain and selected European markets, competing directly with the wealth automation wave that's reshaped how young and middle-class Europeans think about long-term investing. Rather than positioning itself as a replacement for financial advisors—a claim most robo-advisors awkwardly make—Indexa simply assumes you don't need one, and builds a platform on that premise.

The company represents a small but significant shift in European wealth management: proving that passive, rules-based portfolio management can scale, and that investors willing to embrace index-heavy allocations will choose efficiency and transparency over the reassurance of human contact. In that sense, Indexa is less a fintech company and more a philosophical statement about how European investment management should work.

Categories

Wealth