Country

Companies10 of 41

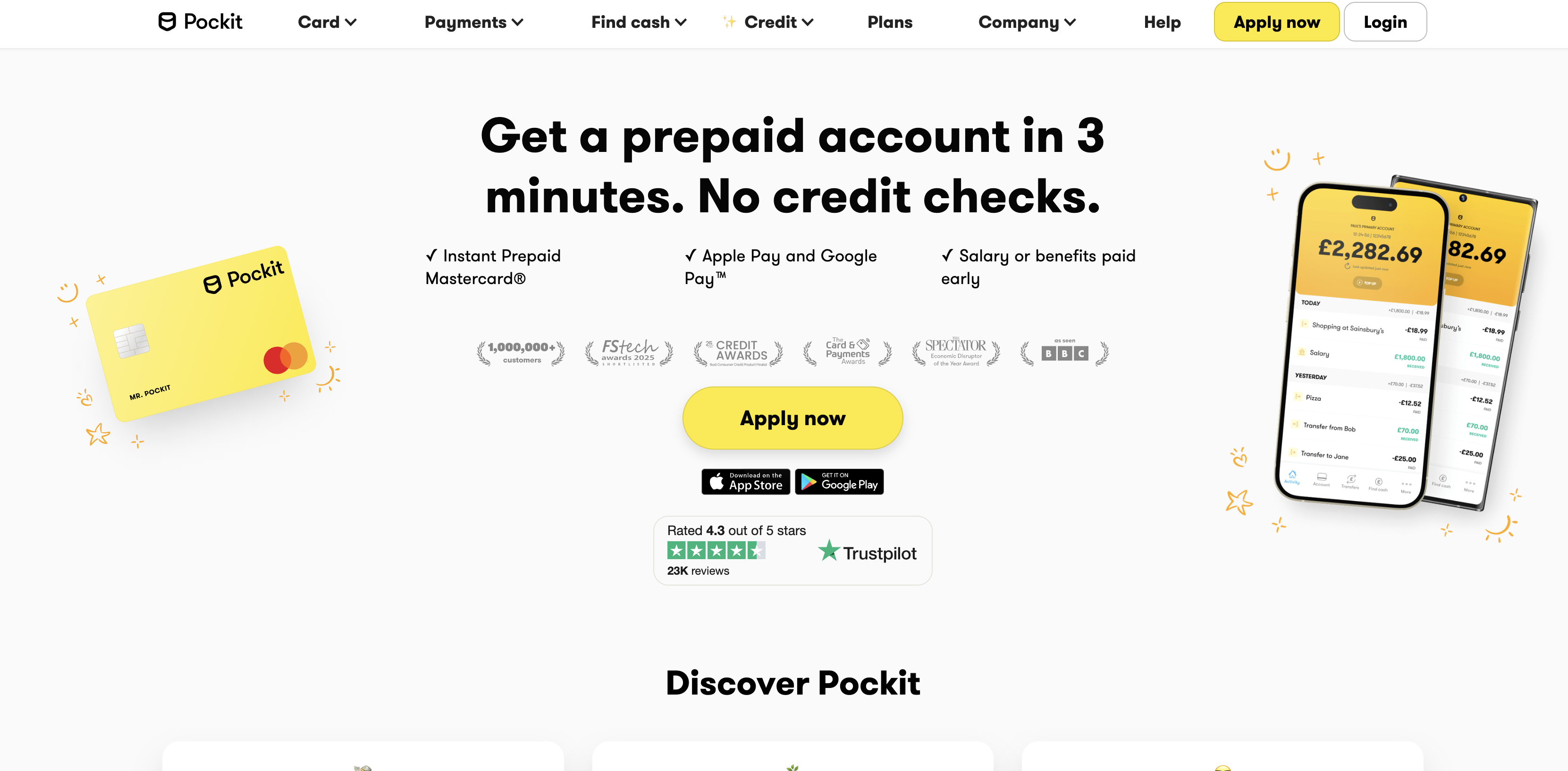

pockit.com

Pockit

pockit.com🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

Categories

Digital BankingPersonal Finance

moneyhub.com

Moneyhub

moneyhub.com🇬🇧 United Kingdom

Open banking's promise — that financial data, properly used, can help people make better decisions — has been articulated by hundreds of companies. Moneyhub has spent longer than most actually delivering it. Founded in Bristol in 2014, it built one of the UK's first and most comprehensive open banking platforms, aggregating financial accounts, pension data, and property values into a unified financial picture that gives users — and the institutions serving them — a genuinely complete view of financial health. Its B2B platform powers the open banking and financial wellness features of major UK employers, financial advice firms, and pension providers, white-labelling its data aggregation and analytics capabilities under their brands. The pensions integration is particularly significant — Moneyhub connects to pension providers alongside bank accounts, giving users visibility into their retirement savings alongside their current financial position. That breadth of financial data coverage — beyond the current account focus of most open banking platforms — is a genuine differentiator. In the UK open banking ecosystem, where the FCA's consumer duty requirements are pushing financial institutions to demonstrate they understand their customers' broader financial circumstances, Moneyhub's comprehensive data view is becoming infrastructure rather than a nice-to-have.

Categories

Open BankingWealthPersonal Finance

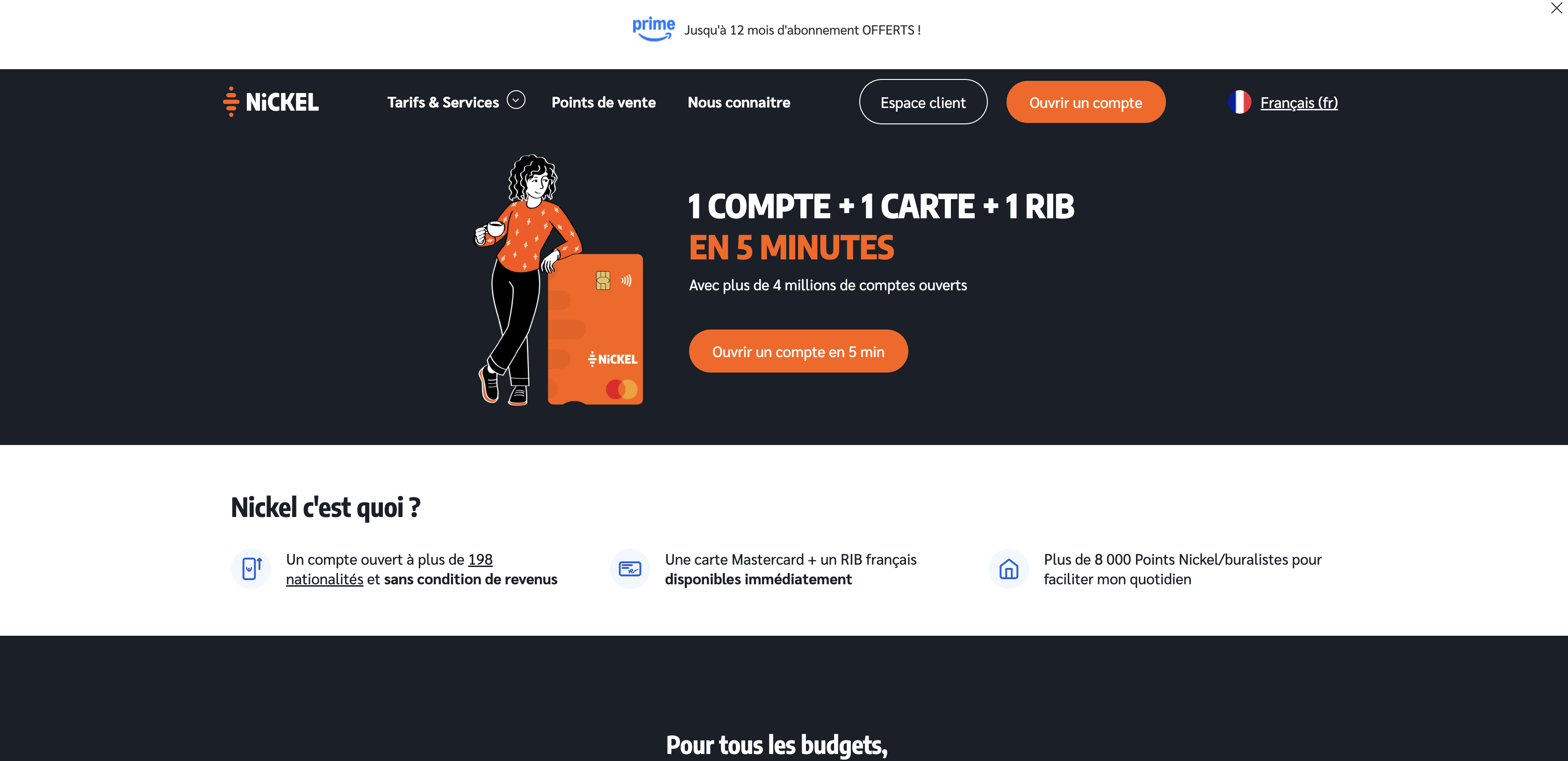

nickel.eu

Nickel

nickel.eu🇫🇷 France

Nickel is a French-born neobank that treats banking as a public good rather than a premium service. It emerged in the early 2010s with a radical premise: everyone deserves access to basic financial tools, regardless of income or credit history. The platform offers no-frills digital accounts, card payments, and essential money management features at a fraction of traditional bank costs.

Unlike the gamified, feature-heavy challenger banks flooding the European market, Nickel stays deliberately minimal. Its appeal lies in straightforward functionality and transparency—no hidden fees, no algorithmic nudges toward credit products, no complexity. The company operates a hybrid model, partnering with physical retailers to provide account opening and cash services, which sets it apart from fully digital competitors.

In the crowded Western European neobank space, Nickel occupies a distinct position: it's inclusive by design, not by accident. While competitors target affluent early adopters with investment tools and lifestyle integrations, Nickel focuses on financial stability for underserved populations—students, gig workers, immigrants, and those excluded from traditional banking. This mission-driven approach has earned it a loyal user base and growing recognition as a serious alternative to incumbent banks.

Nickel represents a quietly powerful force in European fintech: proof that sustainable disruption doesn't require endless feature releases, just genuine accessibility and trust.

Categories

PaymentsDigital BankingPersonal Finance

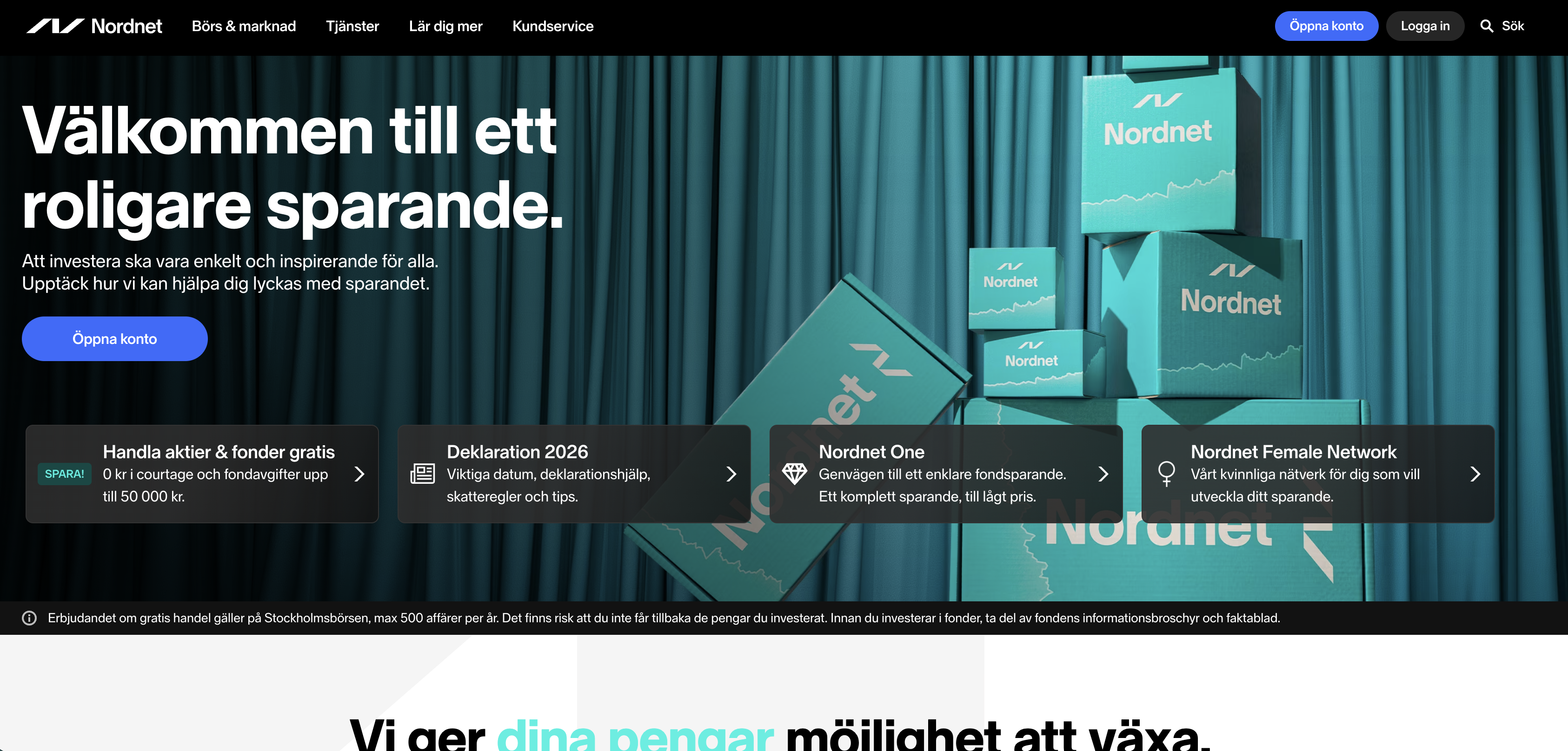

nordnet.se

Nordnet

nordnet.se🇸🇪 Sweden

Pan-Nordic retail investing requires more than translating a Swedish product into Norwegian, Danish, and Finnish. Each Nordic market has its own pension system, tax-advantaged investment accounts, regulatory framework, and consumer expectations — complexity that has kept many investment platforms confined to a single national market. Nordnet was founded in Stockholm in 1996 with the explicit ambition to build a genuinely Pan-Nordic investment platform, and has spent nearly three decades doing it. Its platform serves customers across Sweden, Norway, Denmark, and Finland, offering stocks, funds, ETFs, pensions, and savings products tailored to each market's specific tax-advantaged account structures. The cross-border depth is genuinely unusual — most Nordic financial services companies that operate internationally do so through separate national entities with separate products, rather than the integrated platform approach that Nordnet has built. The company is publicly listed on the Stockholm Stock Exchange and competes directly with Avanza in the Swedish market while occupying dominant positions in several other Nordic countries. In the European retail investment landscape, Nordnet's combination of cross-border integration and decades of operational depth makes it one of the most credible regional brokers in any European market — a model that the rest of Europe has been slower to replicate.

Categories

WealthCapital MarketsPersonal Finance

revolut.com

Revolut

revolut.com🇱🇹 Lithuania

Revolut is a London-born mobile banking platform that turned the idea of a bank in your pocket into reality. It started as a borderless payments app and has evolved into something far more ambitious: a full-stack financial operating system for the smartphone generation. Most traditional banks still treat international transfers as a painful, expensive legacy process. Revolut made them free and instant.

The app combines a debit card, multi-currency accounts, cryptocurrency trading, insurance, and investment tools into a single interface. It's designed for people who spend time across borders, who think in multiple currencies, and who want their financial life streamlined into one place rather than scattered across apps. Founded in 2015, Revolut has grown into one of Europe's most recognizable fintech brands, with millions of active users across the continent. The company operates its own banking licenses in multiple jurisdictions, giving it the regulatory foundation to move fast where traditional banks move cautiously.

What sets Revolut apart is its refusal to accept friction as inevitable. Travel shouldn't require currency conversion fees. Payments shouldn't require knowing IBAN codes. Investing shouldn't require a separate broker account. In the broader fintech landscape, Revolut represents the shift toward unbundled, mobile-first financial services that challenge the notion that banking needs to be complicated.

Categories

Digital BankingPaymentsWealthCrypto & BlockchainPersonal Finance

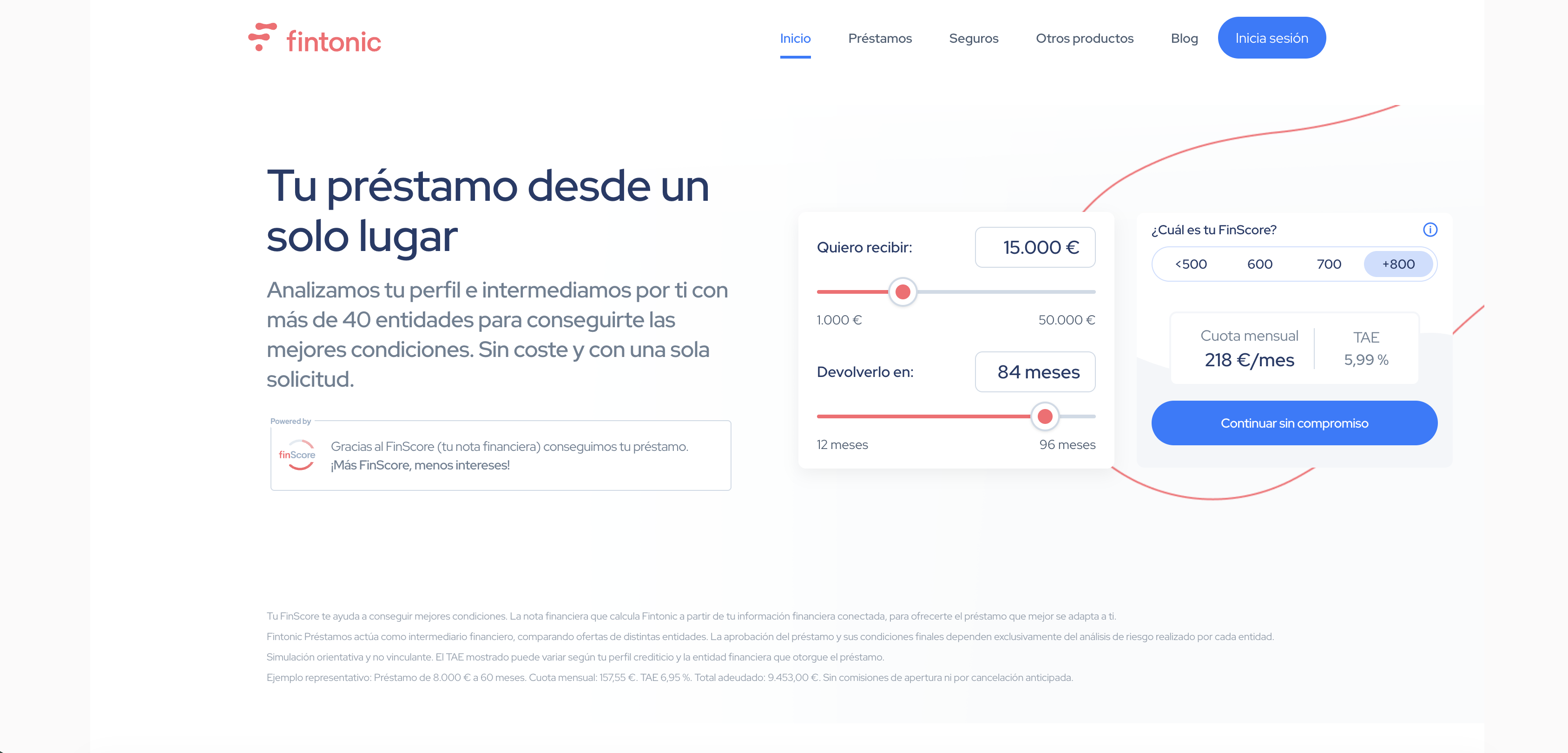

fintonic.com

Fintonic

fintonic.com🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Categories

Personal FinanceOpen Banking

rauva.com

Rauva

rauva.com🇵🇹 Portugal

Rauva is a fintech platform built specifically for small business owners who are tired of juggling spreadsheets and fragmented tools. It combines invoicing, expense tracking, and financial reporting into a single dashboard, giving SMEs real-time visibility into their business finances without the accountant overhead. The platform connects directly to bank accounts and automatically categorizes transactions, turning raw financial data into actionable insights.

What sets Rauva apart is its focus on simplicity and speed. Rather than forcing businesses through complicated setup processes or charging enterprise-level fees, it delivers straightforward features that address the immediate pain points SMEs face: understanding cash flow, managing invoices, and staying on top of tax obligations. The interface feels built for people who run businesses, not for finance professionals.

In the crowded landscape of SME fintech, Rauva competes by refusing complexity. While competitors bundle accounting, payroll, and inventory management into bloated suites, Rauva stays laser-focused on financial visibility and reporting. It's the kind of tool a busy founder pulls up on Monday morning without needing a training session. The company has positioned itself as the alternative to traditional accounting software that feels stuck in the 2000s and overly expensive cloud-based platforms that are overkill for small teams.

Rauva represents the practical middle ground in SME finance: powerful enough to matter, simple enough to use.

Categories

SME FinancePersonal Finance

monzo.com

Monzo

monzo.com🇬🇧 United Kingdom

Monzo is the UK's most downloaded banking app, a fully-fledged digital bank that ditched the branch model entirely and made mobile-first banking feel inevitable rather than experimental. Since launching in 2015 as a prepaid card startup, it evolved into a licensed bank offering current accounts, savings, loans, and investment features—all built around the phone-first thesis that banking should feel less like finance and more like an everyday utility.

What sets Monzo apart in a crowded field of challenger banks is its obsession with transparency and user control. Transaction categorization happens automatically but lets you override it instantly. Spending insights arrive in real-time rather than monthly statements. Customer support happens via in-app chat with actual humans who have context on your account. There's no pretense, no hidden fees, no terms written in legalese—a deliberate stance against how traditional banking communicates.

In Europe's neobank landscape, where dozens of competitors offer slick apps and fast account opening, Monzo has maintained its edge through relentless product iteration and a zealous community of early users. It expanded beyond the UK into Europe, acquiring customer bases in France and Italy, though it remains most mature in its home market. The company went public on the London Stock Exchange in 2023, a rare fintech exit that validated the full-bank model over lighter-weight payment-only plays.

Monzo represents a particular type of fintech success: not a SaaS infrastructure play or a verticalized lending specialist, but rather a consumer-facing bank that proved the regulatory and operational complexity of holding a banking license was worth solving if you could deliver an experience genuinely better than incumbents. It's a reminder that sometimes the fintech opportunity isn't in unbundling banking, but in rebuilding it from first principles.

Categories

Digital BankingLendingWealthPersonal Finance

bitpanda.com

Bitpanda

bitpanda.com🇦🇹 Austria

Bitpanda is a Vienna-based fintech that democratized crypto investing for European retail users who found traditional exchanges intimidating or inaccessible. The platform launched in 2014 as a Bitcoin marketplace and evolved into a multi-asset investment app that lets anyone buy fractions of crypto, stocks, metals, and commodities with a few taps on their phone.

What sets Bitpanda apart is its aggressive focus on the everyday investor rather than crypto enthusiasts. The app strips away complexity, offers micro-investing (you can buy €1 worth of Bitcoin), and integrates savings automation through its Bitpanda Savings feature. It's become a household name in German-speaking Europe, with a clean mobile-first interface that appeals to younger savers who want exposure to alternative assets without the friction of traditional brokerages.

Bitpanda operates across multiple business units: a consumer investment app, an institutional trading platform called Bitpanda Pro, and Bitpanda Elements, its white-label infrastructure play for financial institutions. The company expanded beyond crypto into traditional asset classes to capture a broader addressable market and hedge regulatory risk as European crypto rules tightened.

Among European retail investment platforms, Bitpanda ranks as a serious contender—well-funded, profitable, and operating under tight regulatory scrutiny. It represents a shift in how Europeans think about alternative investments: not as speculative sidebets but as legitimate wealth-building tools accessible to anyone with a smartphone.

Categories

WealthCrypto & BlockchainPersonal Finance

blackcat.app

Blackcat

blackcat.app🇩🇪 Germany

Blackcat is a German fintech platform designed to help freelancers and self-employed professionals manage their finances with minimal friction. Rather than forcing users into complex accounting workflows, Blackcat simplifies the entire money flow—from invoicing to tax filing—with a mobile-first interface that feels more like a consumer app than enterprise software.

The platform tackles a real pain point in the European freelance economy: most existing tools are either bloated legacy systems or fragmented point solutions that don't talk to each other. Blackcat bundles invoicing, expense tracking, tax preparation, and business banking into one coherent experience, removing the cognitive load of juggling multiple services.

What sets Blackcat apart is its opinionated approach to simplicity. Rather than mirroring traditional accounting software's feature sprawl, it prioritizes the workflows that matter most to freelancers—getting paid faster, documenting expenses, and staying tax-compliant without the headache. The platform's integration with German tax authorities and compliance frameworks positions it as particularly valuable in the DACH region, where self-employed taxation can be notoriously complex.

In a market crowded with accounting tools and SME platforms, Blackcat represents a new generation of fintech that starts with the freelancer's actual needs rather than retrofitting legacy processes into a digital wrapper. It's part of a broader shift toward consolidated SME finance platforms that understand that complexity itself is the problem.

Categories

SME FinancePersonal Finance