Country

Companies10 of 10

homecredit.net

Home Credit

homecredit.net🇨🇿 Czech Republic

Home Credit is one of the largest consumer finance operators in Central and Eastern Europe and across multiple emerging markets globally. Founded in 1997 in the Czech Republic by Petr Kellner, the company built its business around point-of-sale consumer credit — financing the purchase of consumer durables, electronics, and increasingly mobile phones in markets where formal banking penetration was lower and where consumers needed credit at the point of major purchases. The company expanded aggressively across Russia, India, Vietnam, the Philippines, China, Indonesia, and other emerging markets, becoming a dominant operator in markets where its physical distribution at retail points of sale gave it advantages that pure digital lenders couldn't match. Home Credit operates at a scale that makes it more comparable to a major regional bank than to the venture-backed fintech startups that dominate fintech press coverage — billions in loans originated, tens of millions of customers, and physical operations across multiple countries. The company has navigated the geopolitical complexity of operating across diverse markets, including significant divestments from Russia following 2022. In the broader European fintech landscape, Home Credit represents an institutional category that exists alongside but separate from the venture-backed startup conversation — a major financial services operator built on operational depth in emerging markets.

Categories

LendingBNPL

montonio.com

Montonio

montonio.com🇪🇪 Estonia

E-commerce growth in Central and Eastern Europe has accelerated significantly through the 2020s, and the payment infrastructure supporting that growth has needed to evolve from supporting basic card acceptance to providing the full range of payment methods, BNPL options, and merchant tools that modern e-commerce expects. Montonio was founded in Tallinn in 2018 to build that infrastructure for the CEE market specifically. Its platform offers payment processing, BNPL integration, and merchant commerce tools designed for Baltic and broader Central European e-commerce businesses, with a particular focus on the integration depth and local payment method coverage that international platforms underserve. The company has grown rapidly across Estonia, Latvia, Lithuania, Poland, and other CEE markets, building merchant relationships and product capability in markets where the e-commerce growth opportunity is significant but where the international payment platforms have not invested with the same depth as in Western Europe. In the European payments landscape, the regional specialist model has shown durable competitive advantages in markets where local payment preferences are distinct, and Montonio represents the new generation of CEE payment infrastructure built for the post-2020 e-commerce environment rather than retrofitted from older payment systems.

Categories

PaymentsBNPLEmbedded Finance

inbank.ee

Inbank

inbank.ee🇪🇪 Estonia

Specialised banking for consumer credit — focused on lending products distributed through merchant partnerships rather than building general-purpose retail banking — is a model with deeper European roots than the venture-backed BNPL conversation suggests. Inbank was founded in Tallinn in 2011 as a specialist lender focused on point-of-sale consumer credit, partnering with retailers across Estonia and the broader Baltic and Central European region to offer instalment finance at the moment of purchase. The company received a full Estonian banking licence and has built operations across Estonia, Latvia, Lithuania, Poland, and the Czech Republic, expanding from a domestic specialist into a Pan-European consumer finance bank. Inbank is publicly listed on the Nasdaq Tallinn exchange — one of the few publicly traded Baltic fintechs — giving it both the regulatory standing of a licensed bank and the funding access of a public company. Its product range covers point-of-sale finance, BNPL, and consumer deposit products, with merchant partnerships across automotive, electronics, home improvement, and other categories where consumers commonly finance purchases. In the European specialist consumer banking landscape, Inbank represents one of the more successful examples of a focused operator scaling across borders while maintaining the operational discipline of a regulated bank.

Categories

LendingBNPLDigital Banking

twisto.cz

Twisto

twisto.cz🇨🇿 Czech Republic

Buy now pay later in Central Europe developed earlier than most Western European observers initially recognised, and Twisto was one of the early Czech entrants in that category. Founded in Prague in 2013, the company built a deferred payment product specifically for Czech consumers, allowing them to receive goods and pay later through a single combined invoice for all their online purchases. The model had clear consumer appeal in a Czech market where credit card penetration was lower than Western European norms but online shopping was growing rapidly. Twisto expanded into payment cards and broader consumer financial services, building one of the more recognisable consumer fintech brands in the Czech market. The company was acquired by Zip, the Australian BNPL operator, in 2022, integrating its Central European operations into a global BNPL group. The acquisition reflects the broader consolidation that has reshaped the European BNPL landscape, with national champions being absorbed into international platforms or struggling to maintain independence as the major players scale across borders. Twisto's trajectory from Czech consumer brand to Zip's CEE entry point illustrates both the genuine consumer demand for BNPL in Central Europe and the difficulty of building independent BNPL businesses at sustainable scale in markets too small to support major standalone operators.

Categories

BNPLDigital Banking

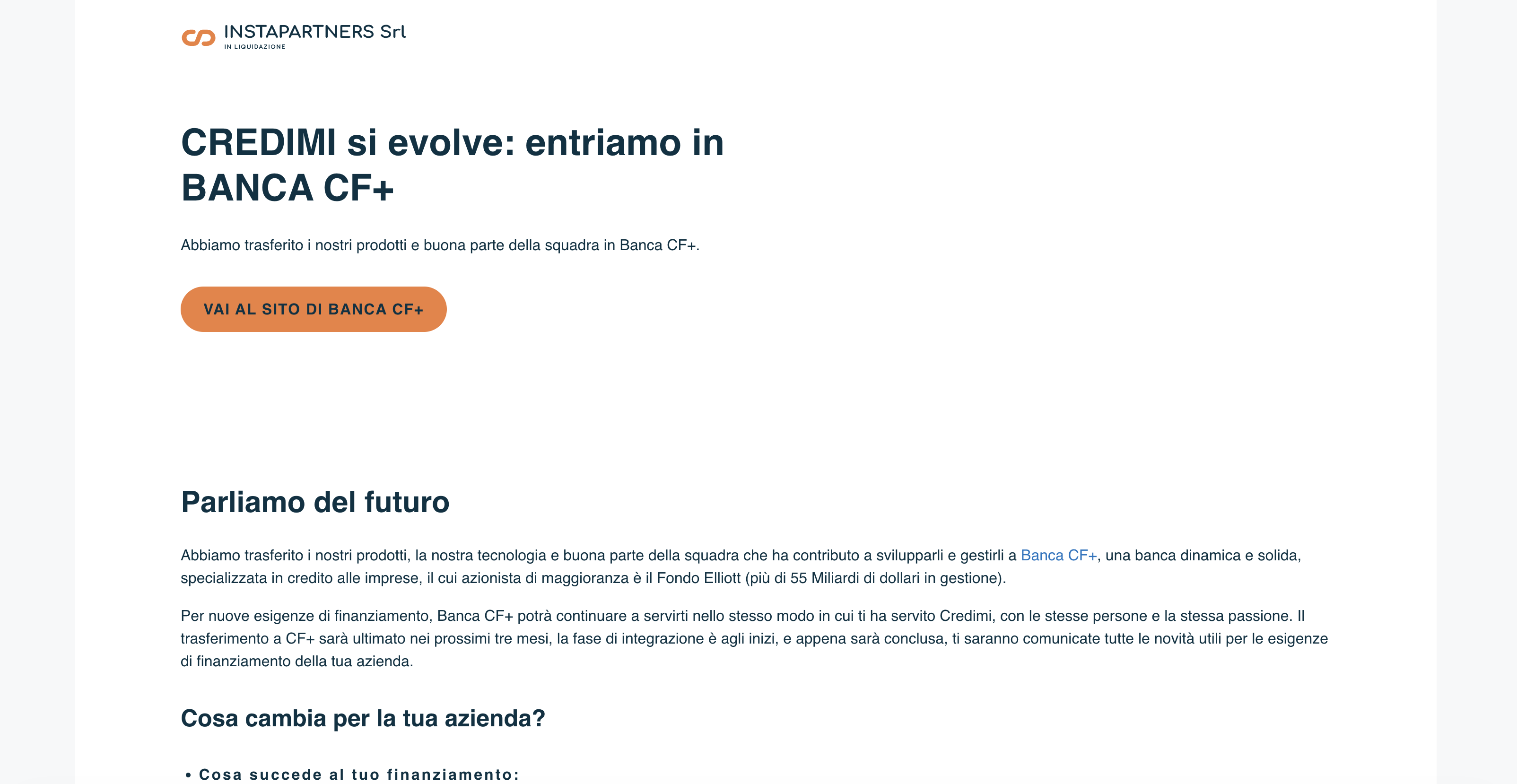

credimi.com

Credimi

credimi.com🇮🇹 Italy

Credimi sits at the intersection of e-commerce and embedded finance, solving a problem that online retailers have largely ignored: making checkout friction disappear. Rather than forcing customers to choose between card payments and bank transfers, Credimi lets shoppers access buy-now-pay-later directly at the point of sale, turning the checkout moment into a financing decision rather than a payment one. The company essentially white-labels installment lending for merchants, handling everything from credit decisioning to collections behind the scenes.

What sets Credimi apart in a crowded BNPL market is its focus on the merchant relationship rather than the consumer one. While competitors chase customer loyalty through branded apps and direct marketing, Credimi takes a B2B approach, embedding its credit engine into partner payment flows and e-commerce platforms. This means retailers get better conversion rates without bearing the customer acquisition cost. The company operates across multiple European markets, particularly strong in the Nordics and DACH region, where fintech-native commerce has matured fastest.

In an industry obsessed with speed and simplicity, Credimi's real edge is its underwriting—it deploys machine learning to make instant credit decisions without the awkward friction of traditional lending. This isn't flashy consumer fintech; it's infrastructure. But it's exactly what online retailers need to compete in markets where BNPL has become table stakes.

Categories

Embedded FinanceBNPL

scalapay.com

Scalapay

scalapay.com🇮🇹 Italy

Scalapay is a BNPL (buy now, pay later) platform built for the European e-commerce market, offering shoppers the ability to split purchases into interest-free instalments at checkout. Rather than simply bolting financing onto existing payment flows, Scalapay positions itself as a full-stack infrastructure play—handling underwriting, risk management, and merchant integration from a single API. The company targets mid-market and enterprise retailers across fashion, electronics, and beauty verticals, regions where instalment purchasing is becoming table stakes for conversion.

What sets Scalapay apart is its focus on merchant flexibility and real-time decision-making. While competitors often impose rigid lending terms or lengthy approval processes, Scalapay emphasizes transparent pricing and instant qualification, allowing merchants to offer financing without friction or hidden costs. The platform integrates seamlessly into checkout experiences—both web and mobile—and provides merchants with detailed analytics on customer behaviour and financing uptake.

Scalapay operates in a crowded BNPL landscape, but differentiates through its emphasis on profitability and sustainable lending rather than growth-at-any-cost customer acquisition. The company has expanded across multiple European markets, particularly in Southern Europe and the Mediterranean, where instalment culture is deeply embedded. Its positioning sits between pure-play consumer lenders and white-label infrastructure providers, serving merchants who want financing capabilities without building their own credit infrastructure.

In the broader fintech ecosystem, Scalapay exemplifies the maturation of embedded finance—moving beyond the novelty of BNPL into building durable, profitable lending platforms that merchants and consumers both trust.

Categories

Embedded FinancePaymentsBNPL

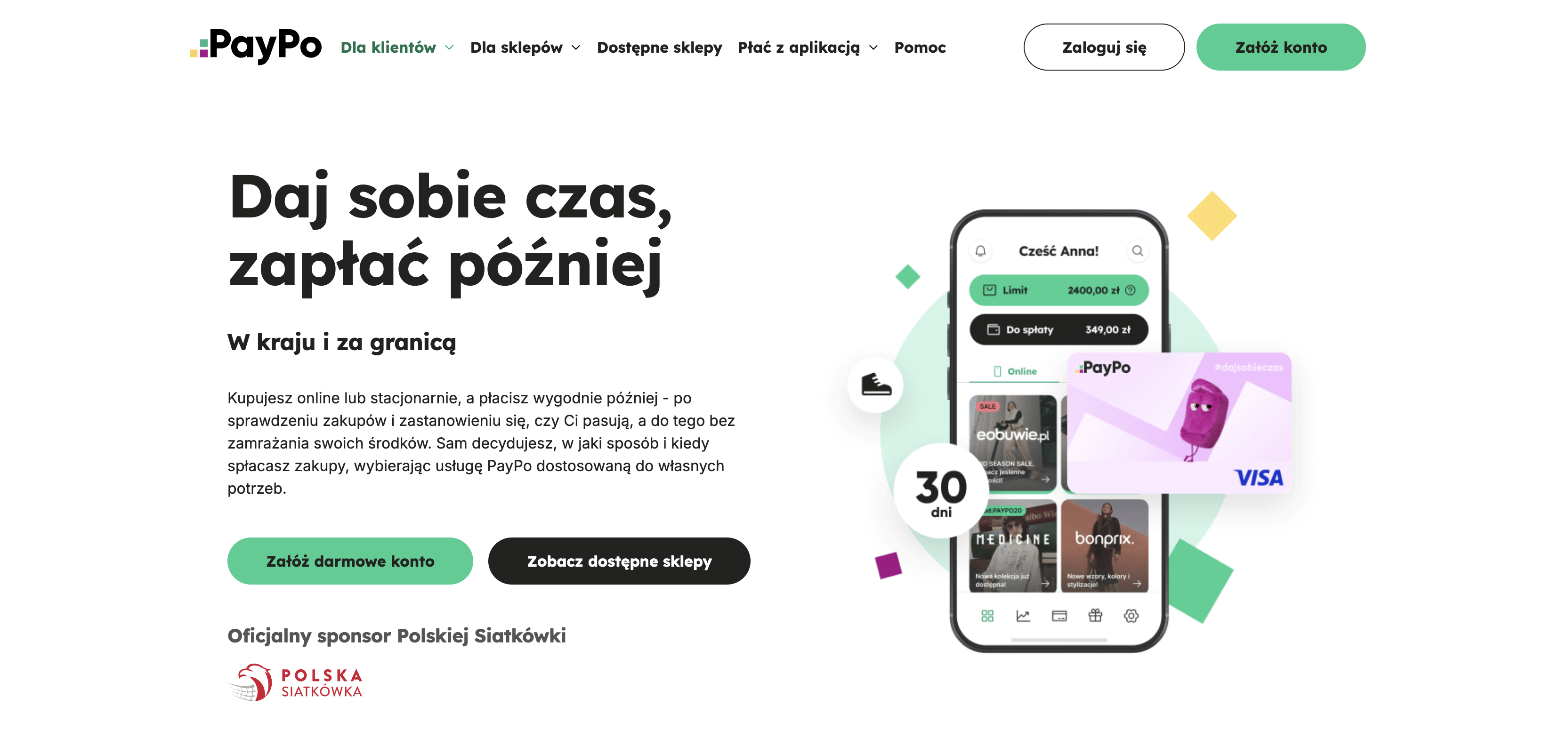

paypo.pl

PayPo

paypo.pl🇵🇱 Poland

Polish buy now pay later developed as a category specifically suited to Polish e-commerce dynamics — high online shopping volumes combined with consumer preferences for deferred payment options that fit the cultural patterns of Polish retail finance. PayPo was founded in Warsaw in 2016 to serve that demand with a BNPL product designed for the Polish market, integrating with Polish e-commerce platforms and offering consumers the ability to receive products immediately and pay later through structured instalment plans. The Polish-first focus has been operationally significant — building merchant relationships, credit underwriting infrastructure, and consumer trust in a single market produces depth that international BNPL platforms have generally not matched in Poland despite the size of the market. PayPo has built one of the more substantial Polish BNPL operations, with merchant integration across the platforms that define Polish online retail and a consumer base that has grown alongside the broader Polish e-commerce expansion. In the European BNPL landscape, where the largest international platforms compete for primary market position across multiple countries, the Polish market has remained a genuinely competitive environment for domestic specialists. PayPo represents the category of national champion BNPL operators that have built sustainable positions through operational focus on a single substantial market.

Categories

BNPLLending

esto.ee

ESTO

esto.ee🇪🇪 Estonia

Estonian consumer credit at the point of online purchase has been transformed by the combination of digital infrastructure that lets credit decisions happen in real time and consumer expectations of completing purchases without leaving the merchant checkout. ESTO was founded in Tallinn in 2016 to serve that specific moment — providing buy now pay later and instalment financing options integrated into Estonian and Baltic merchant checkouts. The platform connects merchants with consumers seeking flexible payment options at purchase, handling underwriting, settlement, and ongoing customer relationship management for the credit products it originates. ESTO has expanded across the Baltic markets and into broader Central European territories, building a position in the BNPL category as one of the regional specialists that competes alongside the larger European platforms by virtue of its local market depth. In the Baltic BNPL landscape, where international platforms have made selective entries but have generally not built the merchant integration depth that domestic operators have, ESTO represents the local champion category. The competitive question for that category is whether local depth in a single regional market can sustain a competitive position as international BNPL platforms continue to expand and as the underlying economics of the category continue to evolve through cycles of growth and regulatory tightening.

Categories

BNPLLending

klarna.com

Klarna

klarna.com🇸🇪 Sweden

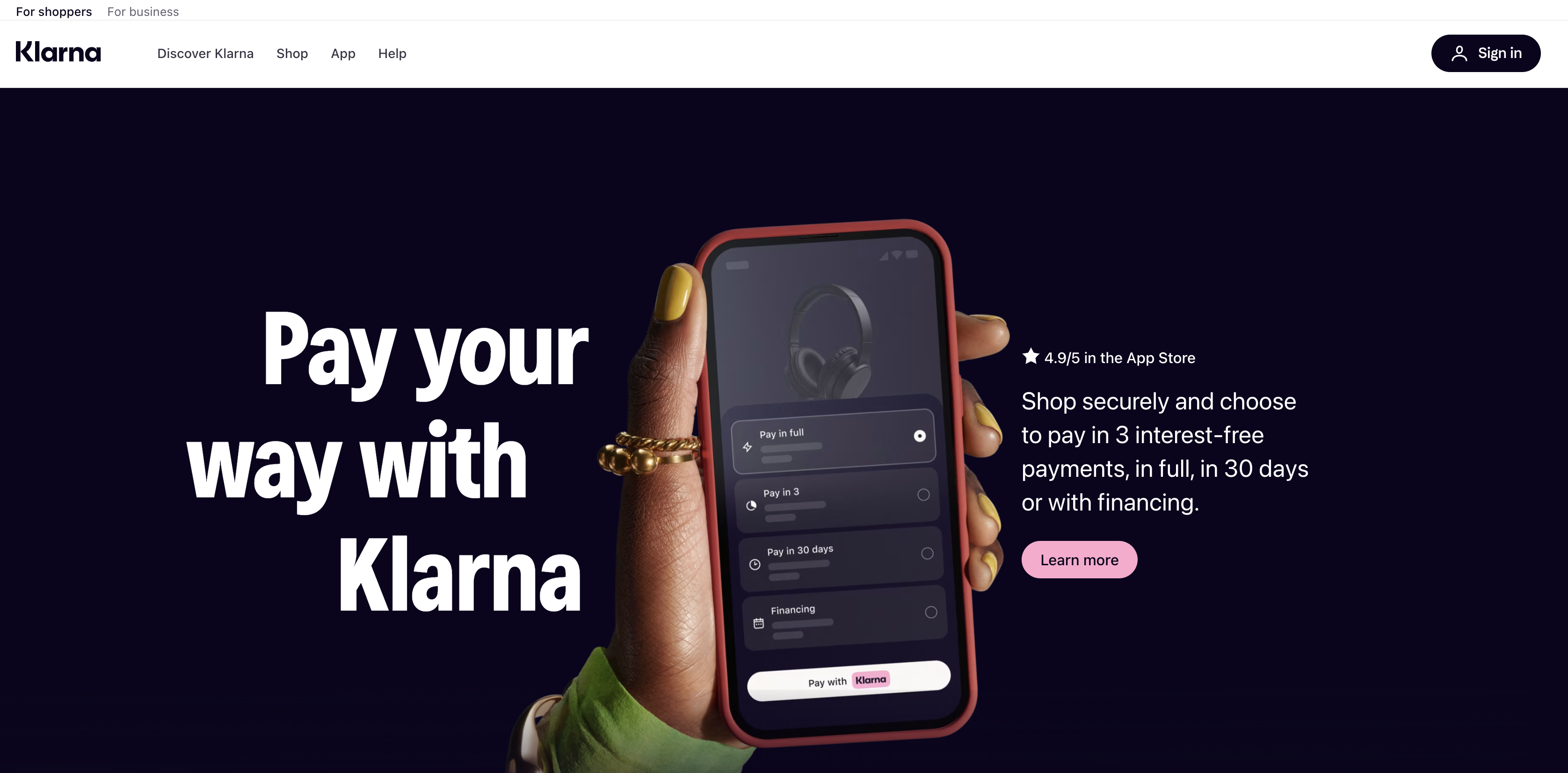

Klarna is the European fintech that made shopping on credit feel frictionless. It started by asking a simple question: why do you need a credit card to buy something online? The answer became a payments platform that lets consumers split purchases into instalments, skip the card altogether, and pay later—without the friction of traditional lending.

The company operates across three overlapping worlds: it's a checkout experience for shoppers, a payments infrastructure for merchants, and increasingly, a full-fledged bank. Consumers use the app to manage their finances across a growing ecosystem of partners, while retailers get a payment method that reduces cart abandonment and increases average order value. Behind the scenes, Klarna runs credit decisioning at scale, onboarding millions of users with minimal friction.

In a market crowded with BNPL competitors, Klarna stands out through sheer reach and merchant relationships. It's available at retailers ranging from Sephora to furniture chains across Europe, the US, and beyond. The company has moved well beyond point-of-sale lending—it now operates a full banking licence in some markets, offers savings accounts, and is building out wealth tools.

Klarna represents a broader shift in European fintech: the blurring of checkout, lending, and banking into a single consumer experience. It's become essential infrastructure for modern retail, reshaping how millions of people think about spending and borrowing.

Categories

BNPLPaymentsDigital BankingEmbedded Finance

narvi.com

Narvi

narvi.com🇫🇮 Finland

Narvi is a European fintech that simplifies embedded lending for e-commerce and marketplace platforms. Rather than forcing merchants to build lending infrastructure from scratch, Narvi handles the entire loan lifecycle—from origination through servicing—as a white-label API that integrates directly into checkout flows.

The company targets online retailers and marketplace operators who want to offer buy-now-pay-later and installment credit without the operational overhead of underwriting, collections, or compliance. Narvi handles credit decisions using proprietary scoring models and manages all regulatory requirements, while merchants simply embed a widget and capture incremental revenue.

In a market crowded with point-solution BNPL providers, Narvi positions itself as a full-stack lending partner rather than a payment mode. The company serves merchants across Europe and has built integrations with major e-commerce platforms, making it simpler for smaller retailers to compete with well-funded rivals on financing offerings.

Narvi represents a growing class of embedded finance infrastructure plays—companies enabling non-financial businesses to offer financial products without becoming financial institutions themselves. Its role is to abstract complexity and regulatory burden, letting merchants focus on customer experience and growth.

Categories

LendingEmbedded FinanceBNPL